Medicare & Retina Emergencies Abroad: Act Now, Organize Later

The scariest part of a retina emergency abroad isn’t the hospital—it’s the moment afterward, when the bill lands and you realize Medicare coverage outside the U.S. is usually a mirage with a few narrow doors.

When flashes, floaters, or a “curtain” shadow hits mid-trip, you’re forced to move fast in a system that doesn’t speak CMS forms or U.S. billing codes. This guide provides a clean, operator-style workflow to help you survive the “paperwork war” and protect your vision.

A standardized benefit in certain Medigap plans that may pay for qualifying emergency care abroad—often 80% after a deductible, only if the emergency begins in the first 60 days of a trip, and capped by a lifetime maximum.

Read this before you need it. Save your future self the paperwork war.

Table of Contents

Safety / Disclaimer (read this first)

This article is educational, not medical or legal advice. Retinal detachment is an emergency—delays can permanently harm vision. If symptoms suggest detachment, seek same-day emergency evaluation by an eye specialist. If you can’t reach ophthalmology quickly, go to an emergency department and request urgent ophthalmology consultation.

Also: I’m going to talk about Medicare, Medigap, and Medicare Advantage in practical, real-world terms. But coverage decisions depend on facts, documentation, and your specific plan rules. When the stakes are vision and five-figure bills, “probably” is not a plan—paperwork is.

1) Act fast first: retinal detachment red flags abroad

“Curtain” symptoms that don’t wait for paperwork

- Sudden shadow or curtain over part of your vision

- New flashes of light

- A sudden burst of floaters (especially if it feels like “snow globe”)

- Sudden vision loss, distortion, or a new “missing area”

When to seek help (no bargaining with time)

If the symptom set suggests detachment, same-day emergency evaluation is appropriate. Retinas don’t care about your itinerary. They also don’t care that your insurer’s call center is closed.

Practical travel reality: in many countries, you’ll be triaged through an ER first, then ophthalmology gets pulled in. Don’t fight that system—use it. Ask (politely, firmly) for “urgent ophthalmology evaluation” and repeat the phrase like it’s your passport.

Operator truth: Your real decision isn’t “coverage vs no coverage.” It’s speed vs regret. The money problem is solved after the retina is stabilized—not before.

- Get evaluated the same day if you can.

- If specialist access is slow, go to the ER and request ophthalmology.

- Assume you may pay upfront, and start collecting documents immediately.

Apply in 60 seconds: Open your phone notes and type the symptom onset time (local time), what changed, and where you are—then save it. That timestamp becomes part of your claim story later.

Composite snapshot #1 (because this is common): A traveler notices a “gray smear” at dinner, tells themselves it’s jet lag, sleeps on it, and wakes up with a bigger shadow. The next morning becomes a scramble of taxis, translations, and last-minute clinic searches. The lesson isn’t shame. It’s workflow: treat the first red flag like an alarm, not a suggestion.

Show me the nerdy details

Retinal detachment risk and urgency vary by type and context (tears vs traction vs exudative processes), and symptoms can overlap with benign issues. That’s exactly why same-day evaluation matters: it’s not your job to diagnose the retina—it’s your job to show up early enough for someone else to do it well.

2) Medicare abroad basics: what “outside the U.S.” really means

The geography trap: territories vs “foreign” (and why this matters)

Medicare’s “outside the U.S.” definition is surprisingly specific. In plain English: the 50 states and D.C. are “inside.” Several U.S. territories are also treated as inside for these rules (for example, Puerto Rico). But most places you think of as “international travel” are, of course, outside—and Original Medicare generally doesn’t cover routine care there.

If you’re reading this at an airport gate, here’s the point: your coverage can change just by crossing a border. The retina emergency doesn’t change, but the payment rules might.

Why billing abroad feels like a different universe

U.S. hospitals typically submit claims to Medicare as part of normal life. Overseas, you may be dealing with a hospital that has never heard the phrase “CMS-1490S,” and they are not obligated to play nice with American administrative systems. Medicare’s own guidance notes that foreign hospitals aren’t required to file Medicare claims—meaning you may have to pay in full, then submit for reimbursement if you qualify.

Composite snapshot #2: Someone gets evaluated in a major European city. The care is excellent. The paperwork is… artistic. One page says “retina problem,” another says “procedure,” and neither shows itemized line items or provider credentials. Clinically fine. Administratively fragile.

Money Block: Are you even in the tiny Medicare “possible” zone?

Answer these yes/no questions. If you’re “no” on all of them, plan on out-of-pocket + Medigap/MA/travel insurance instead.

- Yes/No: Did the emergency happen while you were physically in the U.S., but the closest hospital was across a border?

- Yes/No: Were you traveling through Canada by the most direct route between Alaska and another state, without unreasonable delay?

- Yes/No: Do you live near a border and is the nearest hospital that can treat your condition actually in another country?

- Yes/No: Were you on a ship within the “near a U.S. port” window when services were provided?

Neutral next action: If you answered “yes” to any, start building your documentation pack now and prepare to submit a claim yourself if the provider won’t.

3) The rare Original Medicare exceptions that can pay overseas (the “3 doors”)

Most people think the answer is simply “Medicare never pays outside the U.S.” The more accurate answer is: almost always no—unless you fit one of a few narrow scenarios. Medicare and CMS materials describe three classic foreign-hospital situations where payment may be possible, plus shipboard rules that create a separate category.

Door #1: You’re in the U.S. when an emergency happens, and the foreign hospital is closer

This is the “border-town ambulance” scenario. You’re in the U.S., something urgent happens, and the closest hospital that can treat you is across the border. If you qualify, Medicare may pay for Medicare-covered services tied to that inpatient stay (and associated doctor/ambulance services connected to it).

Door #2: The Alaska–Canada “travel-through” exception

This one is oddly specific and extremely real: if you’re traveling through Canada without unreasonable delay on the most direct route between Alaska and another state, and an emergency occurs, Medicare may pay when the Canadian hospital is closer than the nearest U.S. hospital that can treat your condition. “Without unreasonable delay” is judged case-by-case, which is bureaucratic code for: document your timeline like a grown-up.

Door #3: You live in the U.S., but the foreign hospital is closer than the nearest U.S. hospital that can treat you

This is the “I live near the border and the nearest capable hospital is across it” scenario. It can apply even if it’s not an emergency, but it’s still rule-bound and documentation-heavy.

The ship rule: within a limited time window near a U.S. port

Care on a cruise ship has its own twist: Medicare may cover medically necessary services if the ship is in a U.S. port or within a defined “hours from a U.S. port” window at the time services are provided, and other requirements are met (including whether the doctor is permitted/qualified under certain laws). Once you’re far out at sea, Medicare generally won’t pay.

- Most overseas retinal detachment care will not be covered by Original Medicare.

- If you might fit an exception, the story you document matters.

- Even when Medicare pays something, follow-up abroad often becomes out-of-pocket.

Apply in 60 seconds: Write one sentence you can reuse: “Emergency symptoms began at [time/date], I sought care immediately at the nearest capable hospital.” Then back it up with receipts and timestamps.

Composite snapshot #3: A snowbird near the border gets evaluated across the line because it’s the closest facility with ophthalmology coverage that day. The care isn’t the issue. The issue is proving proximity and necessity: where you were, what options existed, and why this location was medically reasonable.

4) What Medicare won’t pay abroad (even when it’s truly urgent)

“Emergency” doesn’t automatically equal “covered”

Here’s the emotional mismatch that makes people furious (understandably): something can be medically necessary and time-sensitive, and Medicare can still say “not covered” because the care occurred outside the U.S. Coverage rules are not the same thing as medical reality.

Common non-coverage pain points in retinal detachment scenarios

- Follow-up visits abroad: Even if a narrow exception applied to a foreign inpatient stay, the minute you’re outside that episode, coverage often evaporates.

- “Can it wait until I’m home?” decisions: If you delay care and later seek treatment in the U.S., the foreign evaluation might not be reimbursed—and you may have worsened the clinical outcome.

- Packaging and billing styles: Overseas bills may bundle services (facility + surgeon + imaging + supplies) in ways Medicare can’t map cleanly.

- Pharmacy reality: Drugs purchased abroad are typically not covered the way people hope—especially if you’re thinking in Part D terms.

Composite snapshot #4: Someone gets laser or surgery abroad, then stays an extra week “to be safe” and does two follow-up exams locally. The procedure might be the “emergency.” The follow-ups are the gray zone where reimbursement often fails—unless a separate benefit (like Medigap foreign travel emergency or specific Medicare Advantage rules) applies.

Show me the nerdy details

Medicare payment hinges on statutory limits (where services are furnished), benefit categories (Part A vs Part B), and whether the services are considered connected to a covered inpatient stay under an exception. That “connectedness” concept is where many reimbursements die: if the service looks like a standalone outpatient visit abroad, it’s much harder to fit into the rare foreign-coverage boxes.

Money Block: Decision card — treat abroad now vs fly home

This is not medical advice. It’s a practical trade-off frame for time-poor travelers.

- Symptoms suggest detachment (curtain/shadow, flashes/floaters burst).

- You can access urgent ophthalmology faster locally.

- You can pay upfront (credit limit, cash, family help) and document everything.

Cost reality: Higher upfront risk, potentially lower medical risk.

- A qualified clinician has evaluated you and says it’s safe to delay.

- You have a documented plan for immediate care on arrival.

- You’re not gambling with a “maybe it’s nothing” feeling (if you are, read is it just getting older—or a serious eye disease? and stop bargaining with time).

Cost reality: Lower upfront medical bills abroad, potentially higher clinical risk if wrong.

Neutral next action: If you’re undecided, default to evaluation now. You can always decide about surgery timing after a retina specialist looks.

5) Medigap foreign travel emergency: the only predictable safety net (with sharp edges)

If you’re traveling abroad with Original Medicare, Medigap foreign travel emergency benefits are often the most predictable “backup.” Predictable doesn’t mean unlimited. It means: the boundaries are knowable, and you can plan around them.

Which Medigap plans can help (and when it starts)

Foreign travel emergency coverage is included in certain standardized Medigap plans (plan letters vary by what’s sold to new enrollees today, and older plans may still exist if purchased long ago). State insurance departments and Medicare’s Medigap resources can help confirm your exact plan’s benefits. The key is not the letter you think you have—it’s the letter you actually have.

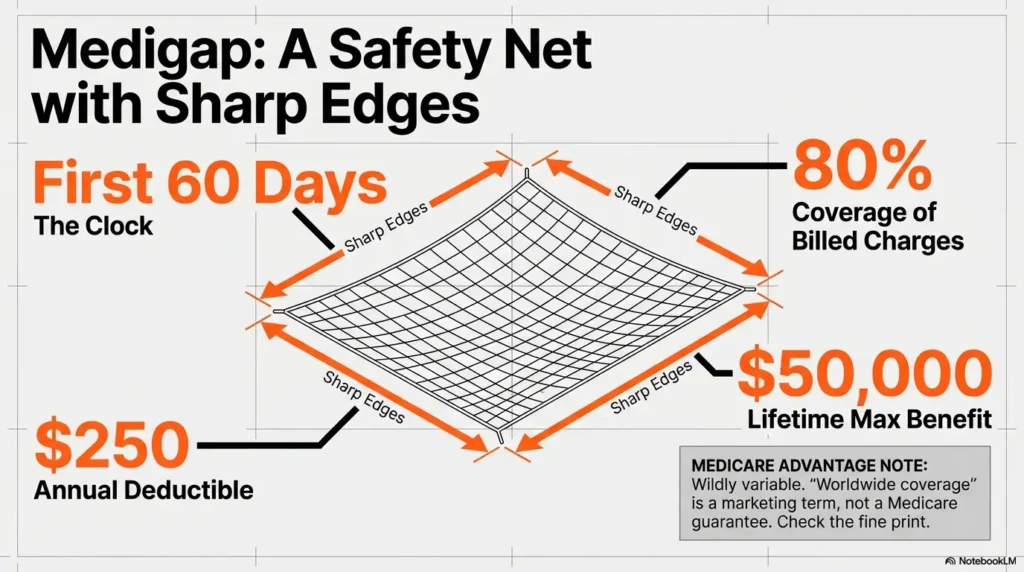

The 4 limits that decide everything

- Time window: Coverage typically applies only if the emergency begins during the first 60 days of a trip.

- Cost share: Many plans pay 80% of billed charges for covered foreign travel emergency care (not 100%).

- Deductible: A separate foreign travel emergency deductible often applies (commonly $250 per year).

- Lifetime cap: A lifetime maximum benefit is common (commonly $50,000).

Money Block: Medigap foreign travel emergency — the benefit in numbers

These are the standardized boundaries many people miss until it’s too late. Confirm your plan’s wording, but plan your cash-flow around these mechanics.

Neutral next action: Before you board, screenshot your Medigap benefits page and save the insurer’s international phone number.

- It often pays 80% after a $250 deductible.

- It usually applies only if the emergency begins in the first 60 days of a trip.

- It often has a $50,000 lifetime cap—treat it like a finite resource.

Apply in 60 seconds: Find your Medigap plan letter and insurer name in your wallet or app and type it into a note titled “Travel Eye Emergency.”

Composite snapshot #5: A traveler assumes, “I have Medigap, so I’m fine.” Then learns mid-crisis that their trip is on day 74, or that the bill has non-covered line items, or that the lifetime cap has already been partially used from a previous incident. Medigap can be a parachute—just don’t assume it’s an infinite one.

6) Medicare Advantage abroad: emergency coverage, “extras,” and the fine print that bites

Medicare Advantage (Part C) plans must follow Medicare rules, but the overseas story is usually: plan-dependent. Medicare’s own materials explain that many MA plans generally don’t cover care outside the U.S., though some offer an extra benefit for emergency and urgently needed services abroad. Translation: the marketing can be generous, the reimbursement rules can be narrow.

What’s typically required (plan-dependent)

- Care must meet your plan’s definition of emergency or urgently needed.

- You may need to notify the plan quickly, even if prior authorization isn’t possible (and if you want a concrete example of how strict this can get in eye care, see Medicare Advantage prior authorization for wet AMD).

- Claims submission requirements can be strict (forms, translations, itemized bills, proof of payment).

Here’s what no one tells you (until you’re holding a receipt)

Even when an MA plan covers overseas emergencies, you may still have to pay upfront and submit for reimbursement—meaning “coverage” is only as good as your documentation and your follow-through after you get home.

Composite snapshot #6: A plan member calls the insurer from abroad and gets a reassuring “Yes, emergencies are covered.” Two months later, the claim is denied because the paperwork didn’t include an itemized bill, the diagnosis wasn’t specific enough, and the dates don’t clearly show it was urgent. The lesson: phone calls comfort you; documents convince reviewers. (If you’ve ever dealt with a denial loop in eye care, the anatomy of a claim denied for an intravitreal injection will feel painfully familiar.)

Show me the nerdy details

Medicare Advantage coverage rules are contract-driven. The same symptom and the same hospital can be treated differently across plans because “worldwide emergency” is not a universal Medicare Advantage requirement—it’s a plan feature with definitions, exclusions, and submission rules. Always read your Evidence of Coverage (EOC) language when possible, or ask the plan to quote the benefit section by name.

7) Who this is for / not for

This is for you if…

- You have Original Medicare (with or without Medigap) and you’re traveling abroad

- You’re in a Medicare Advantage plan and want realistic clarity on overseas emergencies

- You want a claim-ready documentation checklist you can actually follow

Not for you if…

- You want diagnosis or treatment instructions for retinal detachment

- You want a guarantee that Medicare or any insurer will pay (no one can promise that)

If you’re time-poor, here’s your shortcut: act first, document second, submit third. People reverse steps two and three and wonder why reimbursements fail.

She was in Lisbon for three days when the flashes started—tiny camera pops at the edge of her vision. She did what most of us do: blamed the flight, blamed the wine, promised herself she’d “watch it.” By morning, a soft shadow had moved in like a curtain that didn’t fully close but refused to leave. She went to the ER, then ophthalmology, then a small surgical center that asked for payment upfront. Her hands shook signing the card slip.

But she did one smart thing: she kept a thick envelope and stuffed it with everything—intake note, diagnosis sheet, imaging report, the surgeon’s note, the itemized bill, and the card payment receipt. Later, back home, that envelope became her voice when she was too exhausted to argue. The money still hurt. But the story held together. And in reimbursement land, coherence is power.

8) Common mistakes: the 9 ways people lose reimbursement (or pay twice)

Mistake #1: Waiting to “see if it passes”

Medically risky. Also paperwork risky: delayed care can make the timeline look less emergent.

Mistake #2: Paying without getting an itemized bill (and proof of payment)

A single total amount is emotionally satisfying (“paid, done”) and administratively useless. Ask for line items, dates of service, currency, and provider/facility identifiers if possible.

Mistake #3: No diagnosis details (“eye problem” isn’t enough)

You want the clinician’s diagnosis language. “Retinal detachment,” “retinal tear,” “vitreous hemorrhage,” etc. Specificity reduces doubt.

Mistake #4: Missing physician credentials / facility identifiers

Claims reviewers need to know who did what, where. Get names, specialty, clinic/hospital name, and contact info.

Mistake #5: No proof of emergency timeline (onset → evaluation → treatment)

Write it down. Screenshot it. Keep it consistent across documents. (If you want a printable template that makes this painless, use a printable symptom diary as your “timeline spine” and attach it to your claim packet.)

Mistake #6: Not asking for imaging + operative notes when surgery happens

Especially if you had a procedure, you want the operative note and any imaging report. You don’t need a novel—just enough to show what was done.

Mistake #7: Using the wrong claim pathway or missing deadlines

For Original Medicare self-submission, CMS provides the “Patient’s Request for Medical Payment” form (CMS-1490S) with different instruction sets depending on the scenario. Deadlines and submission addresses matter.

Mistake #8: Assuming prescriptions abroad will be reimbursed like U.S. pharmacy claims

Often, they won’t. Treat overseas prescriptions as a separate reimbursement question, not an automatic add-on. (For U.S.-based medication costs later, especially Part B-administered drugs, keep Medicare Part B copay assistance on your radar—different problem, same “don’t assume it’s automatic” lesson.)

Mistake #9: Returning home without a handoff plan (follow-up gaps)

Retina care often involves follow-up. A rushed return without a U.S. appointment plan can create clinical risk and paperwork confusion.

Pattern interrupt: Let’s be ruthless about receipts. If it’s not written down, stamped, dated, and attributable, it may as well not exist when a claim is reviewed.

9) The “evidence pack” to build while you’re still overseas

This section is the difference between “maybe reimbursed” and “clean, convincing claim.” Think of it as building a tiny case file while events are fresh and documents are accessible.

Your one-page checklist (print or screenshot)

- Symptom onset: date/time (local), what changed, which eye

- First evaluation: ER/clinic intake note

- Specialist note: ophthalmology consult note (if available)

- Diagnosis language: the clinician’s wording (not yours)

- Imaging: imaging report (B-scan, retinal imaging, etc.) if provided

- Operative note: if surgery/procedure occurred

- Itemized bill: line items, dates of service, currency, facility and clinician identifiers

- Proof of payment: card receipt, bank record screenshot, cash receipt

- Contact details: phone/email/address for facility and clinician

- Itemized bill + proof of payment are non-negotiable.

- A specific diagnosis phrase beats a vague symptom description.

- Timeline coherence is your quiet superpower.

Apply in 60 seconds: Create one photo album named “Eye Emergency” and drop every document photo into it, in chronological order.

Claim reality: you may need to submit yourself

Medicare materials explain that foreign providers often won’t submit claims to Medicare. If you’re in one of the rare situations where Medicare may pay, you may need to file using CMS-1490S (Patient’s Request for Medical Payment) with the correct instruction set for foreign travel/shipboard scenarios.

Translation strategy that doesn’t break the timeline

- Ask for an English version first (many hospitals can do this, even if it takes an extra day).

- If not possible, translate only the critical pages: diagnosis note, procedure/operative note, itemized bill, discharge summary.

- Keep original language copies. Don’t “replace” documents—add translations as attachments.

Money Block: Quick Medigap estimate (foreign travel emergency)

This is a simple math helper, not a coverage promise. It assumes a typical “80% after $250 deductible” structure and does not account for non-covered items or lifetime cap usage.

Estimated Medigap payment: — | Estimated out-of-pocket: —

Neutral next action: Use this estimate to decide whether you need to raise your card limit or arrange a family transfer—before the hospital asks.

11) Next step: build a “Travel Eye Emergency” card in 20 minutes (one concrete action)

This is the part you can do before the emergency, when your hands aren’t shaking and your battery isn’t at 9%.

Copy/paste this into your phone notes (and keep it pinned)

- Your coverage type: Original Medicare + (Medigap plan letter) OR Medicare Advantage plan name (and if you’re on MA, remember that overseas “coverage” can still be gated by step therapy rules and other contract definitions).

- Member ID(s): plan member number(s)

- Plan phone: include international/collect instructions if your card shows them

- Foreign travel emergency summary: time window, deductible, cap (if Medigap or MA benefit)

- Emergency script: “Suspected retinal detachment—need urgent ophthalmology evaluation.”

- Evidence pack list: itemized bill, diagnosis note, imaging report, operative note, proof of payment

- Emergency contact: one person who can wire funds or raise card limit if needed

One “tiny but mighty” habit: build the story as you go

When you’re exhausted, you’ll forget details. So don’t rely on memory. Add a three-line log like this:

- Onset: [time/date] — what changed

- First care: [time/date] — where you went

- Treatment: [time/date] — what they did + who did it

Get same-day evaluation for curtain/flashes/floaters burst.

Request ophthalmology consult + written diagnosis language.

Photo every document. Get itemized bill + proof of payment.

Write a 3-line timeline (onset → evaluation → treatment).

If needed, use CMS-1490S instructions that match your situation.

Schedule U.S. retina follow-up and keep records consistent.

FAQ

1) Does Original Medicare cover retinal detachment surgery outside the U.S.?

Usually no. Original Medicare generally doesn’t pay for care outside the U.S. except in narrow, rule-bound scenarios. If you’re abroad when symptoms begin, assume you may pay upfront and treat reimbursement as uncertain unless another benefit (like Medigap foreign travel emergency) applies.

2) What are the “exceptions” where Medicare might pay for a foreign hospital?

The classic situations involve proximity and border rules: an emergency while you’re in the U.S. but the closest capable hospital is across a border, travel-through Canada between Alaska and another state under specific conditions, or living near a border where the closest capable hospital is outside the U.S. These are documentation-heavy and not a reliable “travel plan.”

3) Do U.S. territories count as “abroad” for Medicare coverage?

Some U.S. territories are treated differently than foreign countries under Medicare’s “outside the U.S.” definition. Don’t guess—verify based on where you’re traveling (and whether your coverage is Original Medicare or Medicare Advantage with a network/service area).

4) Will Medigap pay for an eye emergency overseas if it happens mid-trip?

It depends on the trip window and your plan’s foreign travel emergency benefit. Many standardized Medigap foreign travel emergency benefits apply only if the emergency begins in the first 60 days of your trip, and they often pay 80% after a $250 deductible, subject to a lifetime cap.

5) What’s the deductible and lifetime limit for Medigap foreign travel emergency coverage?

Many standardized descriptions use a $250 foreign travel emergency deductible and a $50,000 lifetime maximum benefit, with 80% coverage of billed charges for covered emergency care. Confirm your plan’s details and whether you’ve used any of the lifetime maximum previously.

6) Do Medicare Advantage plans cover emergencies abroad automatically?

Not automatically. Medicare Advantage coverage outside the U.S. is typically plan-dependent. Some plans offer an extra benefit for emergency and urgently needed services abroad, but definitions, exclusions, and claim submission rules can be strict.

7) If I pay cash overseas, can I get reimbursed later?

Sometimes—depending on the benefit involved. Foreign providers may not submit claims to Medicare. If you qualify for a rare Original Medicare exception, you may need to submit yourself using the correct CMS-1490S instructions. If it’s Medigap or Medicare Advantage, reimbursement depends on their rules and documentation requirements.

8) What documents matter most for reimbursement?

Itemized bill, proof of payment, diagnosis note with specific language, timeline (onset → evaluation → treatment), provider and facility identifiers, imaging report if available, and operative note if a procedure occurred. Missing any of these can turn a valid event into a weak claim.

9) Should I fly home for treatment if symptoms started abroad?

Only a qualified clinician can advise on medical safety. From a practical standpoint, default to evaluation now. Flying home without evaluation is often a gamble with vision. If you’re told it’s safe to travel, get that recommendation documented and build a plan for immediate care on arrival.

Conclusion

Let’s close the loop from the beginning: your brain does panic and math at the same time. The panic gets you to care. The math keeps your life from being knocked sideways afterward. And in a retinal detachment scenario abroad, the cleanest truth is this: Medicare is rarely the hero overseas. Speed and documentation are. If you have Medigap foreign travel emergency, it can be a real safety net—but it’s bounded. If you have Medicare Advantage, your plan might help—but only as far as its definitions and paperwork allow.

Your best “15-minute next step” is simple: build the Travel Eye Emergency card, screenshot your plan details, and set up a single photo album for documents. That’s not paranoia. That’s preparedness. And preparedness is what lets you treat your vision like the priority it is—without leaving your future self to fight a lonely paperwork war.

Last reviewed: 2026-01-18.