Cataract Surgery and Medicare Part B: What’s Covered and What You Pay Out-of-Pocket – 7 Shocking Cost Traps I Discovered With My Mom’s Surgery

This article was last updated on December 3, 2025.

So, Here’s What I Wish Someone Had Told Me About Medicare Part B and Cataract Surgery

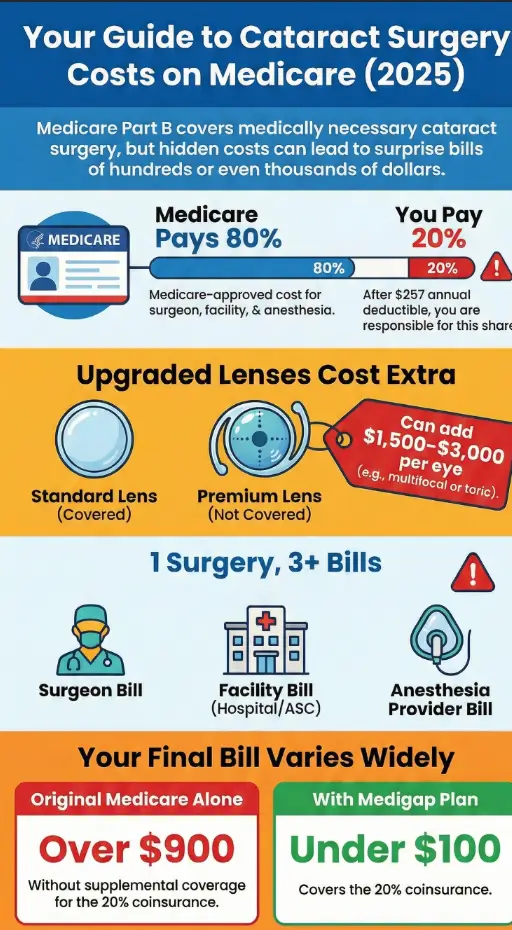

In 2025, the standard Medicare Part B premium is $185/month, and the annual deductible is $257. Once you’ve hit that deductible, Part B usually covers about 80% of the Medicare-approved amount for cataract surgery. Sounds simple, right? You pay the other 20%, plus anything extra for “upgrades” or services Medicare doesn’t cover.

Well, that’s what I thought too.

The morning of my mom’s cataract surgery, I walked into the clinic feeling oddly confident. She had Original Medicare, a Medigap policy, and a color-coded folder containing every letter the federal government had sent her since 1983. I’d done my homework (I thought). What could go wrong?

Turns out: a lot.

By the end of that day, I’d paid three separate bills—from the surgeon, the surgery center, and the anesthesiologist—while also trying to reverse a mysterious charge for a “deluxe” lens neither of us remembered agreeing to. Somewhere between the fluorescent lights and the fine print, I realized: Medicare Part B is not just one benefit. It’s a whole maze—and if you’re not careful, you can overpay by hundreds of dollars before you even get to the recovery room.

So I put this guide together to save you from that fate.

In the next few minutes, you’ll learn what Medicare Part B actually covers when it comes to cataract surgery, where the seven most common cost traps are hiding (spoiler: one is in the waiting room), and how to estimate your real out-of-pocket costs in under a minute—even if all you’ve got is your parent’s Medicare card and a vague sense of panic.

If you’re feeling tired, overwhelmed, and desperately trying to protect your parent’s eyesight without blowing your own budget, trust me: you’re not alone—and you’re exactly where you need to be.

Table of Contents

Part 1 – How Medicare Part B really pays for cataract surgery in 2025

Let’s start with the foundation: what Medicare Part B actually covers when your eye doctor says, “It’s time to take that cataract out.”

In 2025, cataract surgery is usually treated as an outpatient procedure. That means Part B, not Part A, is doing the heavy lifting. After you meet your yearly Part B deductible ($257 in 2025), Medicare generally pays 80% of the Medicare-approved amount for:

- The surgeon’s fee to remove the cataract and implant a basic intraocular lens (IOL)

- The facility costs at a hospital outpatient department or ambulatory surgery center

- Anesthesia services

- Reasonable pre-op and post-op visits related to the surgery

Your 20% coinsurance is based on that Medicare-approved amount, not on whatever sky-high number the sticker price says. If your provider “accepts assignment,” they agree to take the Medicare-approved amount as full payment, which protects you from big surprise markups.

When I finally understood that magic phrase — “accepts assignment” — a lot of the mystery cleared. Before that, I was just nodding through billing conversations like a tired extra in someone else’s movie.

One line that saved us: “Do you accept Medicare assignment for all parts of this cataract surgery, including anesthesia and the facility?”

- Confirm the provider bills under Part B as outpatient.

- Ask every entity (surgeon, facility, anesthesia) if they accept assignment.

- Write down “Part B, 80/20 after $257 deductible (2025)” on your cost sheet.

Apply in 60 seconds: Call the surgery scheduler and ask, “Is all of this billed under Medicare Part B, and do all providers accept assignment?”

The quick math: premiums, deductibles, and typical cataract surgery bills (2025, US)

Numbers first, so you can see the battlefield.

- Standard Part B premium 2025: $185/month for most people (higher if you’re subject to IRMAA based on income).

- Part B annual deductible 2025: $257.

- Coinsurance after deductible: You pay 20% of the Medicare-approved amount for covered services; Medicare pays 80%.

Independent consumer and Medicare-focused resources suggest that the Medicare-approved amount for standard cataract surgery (per eye, outpatient, basic lens) often lands in the ballpark of roughly $2,000–$4,000 depending on region and facility. That’s not a bill; that’s the starting point for the 80/20 split after Medicare’s adjustments.

So, if the approved amount were $3,000 for one eye and you had already met your deductible this year, a very rough sketch looks like:

- Medicare pays about $2,400 (80%).

- You pay about $600 (20%), plus any non-covered upgrades or extra tests.

If you haven’t met your deductible yet, add up to $257 to that out-of-pocket (depending on what you’ve already spent this year on other Part B services).

With my mom, the approved amounts were lower than the terrifying “retail” numbers on the first estimate, but our 20% share still surprised us — especially once we realized we’d triggered a couple of upgrade and “convenience” charges we didn’t strictly need.

Show me the nerdy details

Medicare-approved amounts are based on fee schedules that vary by location and type of facility. Cataract surgery itself is usually coded with CPT codes such as 66984 (routine cataract surgery with IOL) or 66982 (complex case). The facility (hospital outpatient vs. ambulatory surgery center) has its own payment rate, and the surgeon has another. Medicare then applies its fee schedule, and your 20% coinsurance is calculated on that adjusted amount, not on the pre-insurance “charge master” price. If a provider doesn’t accept assignment, they may bill up to a limited amount above the Medicare-approved level, which is why confirming assignment status is so important.

- Look for the phrase “Medicare-approved amount” on estimates.

- Ask for the CPT code and the facility type (ASC vs hospital outpatient).

- Keep 20% of that approved number in your mental budget.

Apply in 60 seconds: Call the billing office and ask, “What’s the Medicare-approved amount you expect for CPT 66984 at your facility this year?”

60-second Medicare cataract coverage check (Money Block)

Before we dive into horror stories, let’s confirm whether your situation is actually in cataract-surgery territory and how Part B likely sees it.

Money Block #1 – Eligibility checklist

Yes/No questions:

- Has an ophthalmologist (MD/DO) diagnosed a cataract that significantly impairs vision in daily activities (driving, reading, work)?

- Is the surgeon Medicare-enrolled and willing to bill Part B?

- Is the planned surgery outpatient (hospital outpatient or ambulatory surgery center) or in-office with appropriate equipment?

- Is the planned lens at least a standard monofocal IOL (not only a cosmetic upgrade)?

- Do you have active Medicare Part B coverage in the month of surgery?

If you answered “Yes” to all: you’re in the typical bucket where Part B covers medically necessary cataract surgery, minus deductible and coinsurance.

If any “No” shows up: ask the surgeon directly, “Can you document this as medically necessary for Medicare Part B? If not, can I see a written estimate of my private-pay cost?”

Apply in 60 seconds: Circle yes/no on each line for your situation and note the one question that feels shaky. That’s your first phone call this week. Save this table and confirm the current rules on the official Medicare site before you schedule.

Part 2 – The 7 shocking cost traps we hit with my mom’s surgery

Here are the land mines we stepped on with my mom’s cataract surgery — plus a few I only discovered after talking with other families, surgeons, and insurance reps.

Trap 1 – Assuming “Medicare covers everything” for cataract surgery (2025, US)

The biggest trap is psychological. “Medicare covers it” often gets translated in the brain as “I won’t owe much.” In reality, even when Medicare Part B is doing its job perfectly, you still face:

- The annual Part B deductible (up to $257 if you haven’t met any of it yet).

- 20% coinsurance on the Medicare-approved amounts.

- Potential copays or facility fees, especially in hospital outpatient settings.

With my mom, we were lulled by the phrase “fully covered” in a casual conversation. That was technician shorthand for “covered under Medicare,” not “$0 out-of-pocket.” The actual bill — about $480 after her Medigap plan stepped in — was fair, but not what we had in our heads.

How to disarm this trap: any time someone says “covered,” translate it in your notes to “Part B 80/20 after deductible; what is my estimated 20% here?”

Trap 2 – Premium lens upgrades (multifocal, toric) that Part B won’t fully cover

Medicare Part B generally covers a basic monofocal lens implant if it’s medically necessary. The moment you move into “deluxe” territory — multifocal lenses, extended-depth-of-focus lenses, advanced astigmatism correction beyond the standard — you’re entering a cost-sharing gray zone.

What often happens in the real world:

- The base cost of a standard lens and its implantation is covered under Part B.

- The “upgrade” portion (the difference between basic and premium) is billed directly to you as an out-of-pocket charge.

- That upgrade can easily run $1,500–$3,000 per eye, and Medicare won’t change its payment just because you chose the fancier option.

We almost agreed to a premium lens for my mom because the surgeon’s assistant described it as “your one chance to fix everything at once.” It was only when I asked, “Exactly how much of this is out-of-pocket and what part is actually Part B–covered?” that she admitted the upgrade would be 100% our responsibility.

“Write down the code for the basic lens and the code for the premium lens, then ask what Medicare approves for each. Your decision may change once you see those two numbers on paper.”

Trap 3 – Pre-op tests that Part B may not see as “medically necessary”

Modern cataract surgery planning can involve a buffet of eye measurements: optical coherence tomography (OCT), corneal topography, advanced biometry, and more. Some are essential for a safe, accurate result; others are nice-to-have upgrades.

Part B generally covers tests that are medically necessary for diagnosing or treating a condition. But if your surgeon’s office has a “premium package” of extra imaging bundled with fancy lenses, those add-ons can end up in the not-covered or partly-covered column.

When I saw a $260 “diagnostic package” on my mom’s estimate, I asked which tests were required for Medicare and which were optional. The scheduler crossed out one line item immediately and said, “Right, you don’t actually need that for a standard lens.” That one question saved us enough to pay for her new sunglasses later.

- Ask for each test’s name and whether it’s needed for a standard lens.

- Request a separate written price for optional imaging.

- Skip bundles you don’t understand until someone explains them line by line.

Apply in 60 seconds: Email or call the office: “Can you highlight which pre-op tests are Medicare-required for a standard IOL and which are optional upgrades?” Save that list and confirm the current fee schedule with the provider.

Trap 4 – Facility choice (ASC vs hospital outpatient) that changes your 20%

Cataract surgery can happen in:

- An ambulatory surgery center (ASC)

- A hospital outpatient department

- Occasionally, a properly equipped office-based surgery suite

The Medicare-approved amount is often lower in ASCs than in hospital outpatient departments, which means your 20% is smaller, too. In some regions, the difference can be several hundred dollars per eye, even with Medicare paying 80% of each setting’s own approved rate.

My mom’s surgeon operated at both a hospital and an ASC. The estimate for the hospital outpatient setting was about 25% higher than the ASC — same surgeon, same lens, same anesthesia group. Nothing about her health required a hospital outpatient setting. We moved her surgery to the ASC and watched the projected coinsurance drop accordingly.

Key question: “Does my eye or medical history require a hospital outpatient setting, or is an ASC safe and available — and what’s the estimated Medicare-approved amount in each location?”

Trap 5 – Anesthesia and pathology that show up as surprise separate bills

In theory, you know anesthesia and any tissue analysis will cost something. In practice, a lot of people are still shocked when they get entirely separate bills from:

- The anesthesia group

- A pathology lab (if any lens capsule or tissue is sent)

Medicare Part B may still apply the same basic pattern — deductible, then 80% coverage of approved amounts with you paying 20% — but if the anesthesia provider doesn’t accept assignment or is out-of-network for your supplemental coverage, your share can jump unexpectedly.

In my mom’s case, the anesthesia group did accept Medicare assignment, but they billed under a different tax ID I didn’t recognize. For two days I was convinced we’d been scammed. We hadn’t — but it reminded me to always ask, “Who else will bill us separately for this surgery?”

Trap 6 – Post-op glasses, drops, and follow-ups that don’t feel like surgery costs (but are)

Medicare Part B often covers one pair of post-cataract glasses with standard frames or a set of contact lenses after cataract surgery that implants an IOL, but anything beyond that — designer frames, second pairs, blue light filters — is generally on you. Meanwhile, the prescription eye drops (antibiotics, anti-inflammatories) can add $100–$300 per eye depending on brand, insurance, and pharmacy.

We felt this one right away. The surgery itself was manageable; the sticker shock came at the pharmacy. Only after I asked the surgeon about generics and “combo” drops did we find a more affordable regimen that was still safe for her.

Pro tip: ask your surgeon for the medication plan two weeks before surgery and shop prices at multiple pharmacies (especially if you have Part D or another drug plan).

Trap 7 – Ignoring Medigap, Medicare Advantage, and IRMAA until it’s too late

If you have Original Medicare plus a Medigap plan, that supplement may cover much or all of your 20% coinsurance for cataract surgery, depending on the plan letter and whether the provider participates. If you’re on a Medicare Advantage plan (Part C), your out-of-pocket might be structured as a fixed copay (for example, a set amount per surgery) instead of 20% coinsurance — but only if you stay within the plan’s network.

Meanwhile, higher-income retirees can be hit with IRMAA (an income-related surcharge) that increases their Part B and Part D premiums by hundreds of dollars per month, even before surgery enters the picture.

Short Story: When we finally sat down with my mom’s Medigap booklet at the kitchen table, we realized her Plan G filled the Part B coinsurance gap almost completely for covered services. In real numbers, that meant her 20% share of the surgeon and facility bills for cataract surgery dropped from about $620 to under $100 total, mostly from non-covered extras and drug costs. A week later, my friend’s dad had surgery with only Original Medicare — no Medigap, no Advantage, just Part A and B — and his out-of-pocket for a similar procedure cracked $900. Both were “covered,” but their coverage tiers and supplemental choices completely changed the bill.

- Confirm if you have Original Medicare + Medigap or a Medicare Advantage HMO/PPO.

- Ask each plan how cataract surgery is coded and what your share is.

- Note any IRMAA surcharges so you’re not surprised by premium jumps.

Apply in 60 seconds: Grab your Medigap or Advantage card and call the number on the back: “What would my estimated out-of-pocket be for standard cataract surgery with an IOL this year?” Save their answer and confirm against your written fee schedule.

How Medigap, Medicare Advantage, and employer plans change your bill

This is where the “coverage tiers” mindset helps. Think of your situation as one of these five tiers:

- Original Medicare only (Part A + B): pay premium + deductible + 20% coinsurance on approved amounts.

- Original Medicare + Medigap Plan G/N: premium + deductible; 20% coinsurance often largely absorbed by the supplement.

- Medicare Advantage HMO with in-network surgeon: premium (sometimes $0) + fixed copay or percentage for surgery; strict network rules.

- Medicare Advantage PPO with out-of-network surgeon: higher copay/coinsurance; more unpredictable bills.

- Original Medicare + retiree or employer coverage: complex coordination of benefits; sometimes better drug coverage.

Region matters too. In the US, Medicare rules are federal, but the actual approved amounts can differ by ZIP code and facility. A hospital outpatient department in a high-cost urban area will often carry higher approved fees than an ASC in a smaller city, even under the same Part B rules.

Money Block #2 – Coverage tier map (Original Medicare vs Medigap vs Advantage, 2025)

- Tier 1 – Original Medicare only: Estimate 20% of approved amounts + deductible. Budget on the higher side.

- Tier 3 – Original + Medigap Plan G: After deductible, Medigap often pays most Part B coinsurance for covered services.

- Tier 5 – Medicare Advantage HMO in-network: Often a fixed copay per surgery, but only if using in-network providers and facilities.

Ask your insurer for a one-page explanation of cataract surgery coverage under your specific plan and year. If the answer feels vague, escalate and ask for the “benefits summary” that lists cataract surgery or outpatient surgical procedures explicitly.

Apply in 60 seconds: Circle your tier, then write a number next to it: “My estimated cataract surgery share is around $____ per eye.” Save this table and verify against your plan’s 2025 benefits booklet.

Money Block – 2025 cataract surgery fee table you can screenshot

Use this as a starting point only. Real numbers depend on region, facility, and your exact coverage.

| Item | Example Medicare-approved amount (2025) | Your share with Original Medicare (after deductible) | Your share with Medigap Plan G (typical) |

|---|---|---|---|

| Surgeon fee (CPT 66984) | $900 | $180 (20%) | $0–$20 |

| Facility fee – ASC | $1,200 | $240 (20%) | $0–$40 |

| Anesthesia | $400 | $80 (20%) | $0–$15 |

| Premium lens upgrade (optional) | $1,800 | $1,800 (not typically covered) | $1,800 (often still on you) |

Example only, not a quote. Use this to frame questions for your actual providers.

Money Block #3 – Mini estimator (paper-and-pen version)

- Ask for the total Medicare-approved amount for your cataract surgery (surgeon + facility + anesthesia) per eye: A = $______

- Estimate your 20% coinsurance: B = A × 0.2 = $______

- If you haven’t met your Part B deductible, add the remaining portion (up to $257): C = $______

- Subtract what your Medigap or Advantage plan says it will pay: D = $______

Your rough share ≈ B + C − D.

Apply in 60 seconds: Plug in approximate numbers from your estimates using this formula. Save it, then confirm each line with your provider’s billing office and your insurance plan.

Part 3 – Scripts, checklists, and phone calls to make before surgery

At this point, you know the structure: premium, deductible, 80/20 coinsurance, and the seven traps. Now we turn that into a short list of conversations you can actually have this week.

Script 1 – Calling the surgeon’s office

You: “Hi, my name is _____. I’m calling about my (or my mom’s) upcoming cataract surgery. Can I ask a few questions about how this is billed under Medicare Part B?”

Questions to ask:

- “Is the surgery billed as outpatient under Medicare Part B?”

- “Do the surgeon and facility both accept Medicare assignment?”

- “Can you share the expected Medicare-approved amount for this surgery this year?”

- “Which pre-op tests are required for Medicare, and which are optional extras?”

- “Is any part of this a premium or deluxe lens upgrade? If so, what is that portion’s exact cost?”

Script 2 – Calling your Medigap or Medicare Advantage plan

You: “Hi, I have a question about how cataract surgery is covered this year.”

Questions to ask:

- “I have Medicare and [Plan Name]. For standard cataract surgery with an IOL, what is my expected out-of-pocket per eye?”

- “Is it a flat copay or a percentage? What’s the limit?”

- “Does the surgeon and facility I’m using count as in-network?”

- “Do you cover the 20% coinsurance after Medicare for surgeon, facility, and anesthesia?”

- “Does my plan include any extra vision benefits or discounts for glasses after surgery?”

Money Block #4 – Quote-prep list

Before you start calling, gather:

- Medicare card (red, white, and blue)

- Medigap or Medicare Advantage card

- List of medications and diagnoses (especially diabetes, glaucoma, macular degeneration)

- Proposed surgery date and eye (right vs left)

- Surgeon name, facility name, and any CPT codes they provided (like 66984)

Apply in 60 seconds: Drop these five items into a folder or notes app titled “Cataract Surgery 2025.” It will save you 20–30 minutes of shuffling during phone calls.

Infographic – your cataract surgery money map in one glance

Cataract Surgery Money Map (2025, US)

1. Before surgery

- Confirm diagnosis + medical necessity.

- Check Part B status, deductible left.

- Choose facility (ASC vs hospital outpatient).

- Verify Medigap/Advantage coverage.

2. Day of surgery

- Standard vs premium lens decision.

- Know who will bill you (surgeon, facility, anesthesia).

- Keep a simple cost sheet in your bag.

3. After surgery

- Fill drops at best-price pharmacy.

- Order Medicare-covered glasses (1 pair).

- Match each bill to your estimates.

- Appeal anything that doesn’t match codes.

Use this map as a one-page dashboard: print it or screenshot it, then write your own numbers in the empty spaces.

FAQ

1. Does Medicare Part B fully cover cataract surgery?

No. In 2025, Part B generally covers 80% of the Medicare-approved amount for medically necessary cataract surgery after you’ve paid the annual Part B deductible ($257). You’re responsible for the remaining 20% coinsurance and any non-covered extras like premium lenses or optional tests. A Medigap plan may cover some or all of that 20%, depending on the plan.

60-second action: Call your plan and ask, “For standard cataract surgery in 2025, what is my estimated out-of-pocket per eye?”

2. How much will cataract surgery cost me out-of-pocket with Original Medicare only?

There is no single number, but a common pattern in 2025 is: you pay up to the $257 Part B deductible (if not already met) plus about 20% of the Medicare-approved amounts for the surgeon, facility, and anesthesia. For many people, that ends up in the low-to-mid hundreds of dollars per eye, but it can be higher if approved amounts are higher in your area or if you choose premium options.

60-second action: Use the mini estimator above with the real approved amounts from your surgeon’s office.

3. Does Medicare pay for glasses after cataract surgery?

Medicare Part B typically helps pay for one pair of eyeglasses with standard frames or one set of contact lenses after cataract surgery with an IOL. Anything beyond that — designer frames, multiple pairs, certain coatings — is usually out-of-pocket. Your supplemental or Advantage plan may add extra vision benefits, so it’s worth checking both.

60-second action: Before surgery, ask your plan, “Where should I go to get my post-cataract glasses, and what will I pay?”

4. What if I can’t afford the coinsurance for cataract surgery?

If the 20% share is too high, start by asking the provider’s billing office whether they offer payment plans. If your income is limited, you may qualify for a Medicare Savings Program or Medicaid, which can help pay premiums and cost-sharing for Medicare. Some nonprofit hospitals and clinics have financial assistance or charity care policies, even for insured patients.

60-second action: Call your state’s SHIP (State Health Insurance Assistance Program) and say, “I’m struggling with cataract surgery costs. What programs can help cover Medicare premiums and cost-sharing?”

5. What happens if my cataract surgery claim is denied by Medicare?

Denials can happen if documentation doesn’t clearly show medical necessity or if coding is off. You have the right to an appeal, starting with a redetermination request from the Medicare Administrative Contractor. Ask your surgeon’s office to provide medical records and a letter explaining why the surgery was necessary (impact on driving, reading, work, or safety). If you have an Advantage plan, follow that plan’s internal appeal process first.

60-second action: If you receive a denial notice, highlight the reason code, then call the surgeon’s billing office and ask, “Can you walk me through how we appeal this specific denial together?”

Final 15-minute checklist before you book the surgery

Let’s close the loop from that first hectic morning with my mom.

Once we slowed down and treated cataract surgery as both a medical decision and a small financial project, everything felt lighter. The same Medicare rules that first looked impossible turned out to be fairly predictable once we knew which questions to ask and which traps to sidestep.

- ✅ Confirm medical necessity and that your surgeon and facility accept Medicare assignment.

- ✅ Get written estimates that include Medicare-approved amounts and your estimated share.

- ✅ Decide in advance whether premium lens upgrades are worth the full, out-of-pocket cost.

- ✅ Use the mini estimator to sanity-check every bill that arrives.

- ✅ Keep that money map infographic handy so you always know where you are in the process.

- Lock in this year’s deductible and coinsurance pattern.

- Compare coverage tiers before you agree to upgrades.

- Match every bill back to a code, an estimate, and a plan.

Apply in 60 seconds: Pick one phone call — surgeon, plan, or pharmacy — and make it today. Capture their answers in your “Cataract Surgery 2025” folder so the rest of the process feels like following a checklist, not dodging surprises.

Last reviewed: 2025-12; sources: Medicare.gov, Centers for Medicare & Medicaid Services (CMS), and major Medicare plan providers.

If you’re reading this in a later year: Medicare costs change annually. For example, 2026 Part B premiums and deductibles are already scheduled to rise again. Always confirm the current year’s numbers on the official Medicare site or with your plan before relying on any estimate.

cataract surgery and Medicare Part B, Medicare cataract surgery costs 2025, cataract surgery out-of-pocket estimate, premium lens upgrade Medicare, Medigap vs Medicare Advantage cataract coverage