Who Is ‘High Risk’ for Glaucoma on Medicare? Diabetes, Family History, and Coverage Rules Explained – 7 Costly Mistakes I Sadly Learned the Hard Way

You can be “high risk for glaucoma on Medicare” for years without anyone saying the words out loud.

I learned that the hard way—after missing screenings I qualified for, mis-booking visits, and paying for tests that should’ve been predictable. It wasn’t vision loss that caught my attention; it was a single line on my paperwork that quietly changed everything.

Glaucoma doesn’t tap you on the shoulder. It erases nerve fibers long before a blind spot ever shows up, and Medicare’s high-risk rules only help if you understand how diabetes, family history, or age-ethnicity factors shape both your risk and your bill. Miss the timing or the coding, and you don’t just risk your eyesight—you risk paying more for less clarity.

- To see whether you actually qualify.

- To understand what Medicare really pays for.

- To avoid the seven mistakes most people don’t notice until it’s expensive.

- To ask sharper questions in a rushed exam room.

Table of Contents

Why “high risk for glaucoma on Medicare” matters more than you think

“High risk” sounds like a label for other people—until you realize it’s Medicare’s way of saying, “We’ll help you pay to catch glaucoma early, but only if you fit our checklist and use it correctly.”

Glaucoma is sneaky. You can lose up to 40% of nerve fibers before you notice a problem in daily life. By the time you’re bumping into door frames or squinting at road signs, you’ve already lost vision you can’t get back. The entire point of the high-risk benefit is to pay for regular, dilated exams with optic nerve and pressure checks so that damage is caught while there’s still something to save.

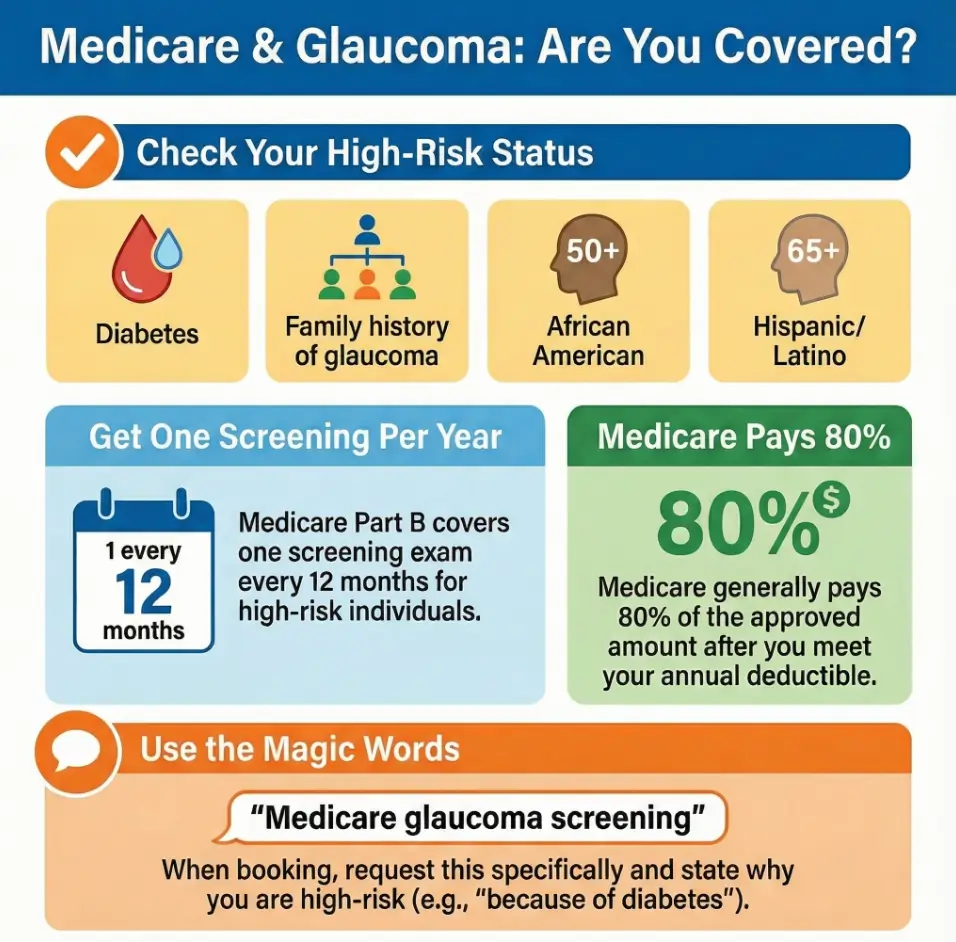

On paper, the deal is good: if you meet Medicare’s high-risk criteria, Part B generally pays 80% of the approved amount for a glaucoma screening after you meet the annual deductible, and you pay the remaining 20% or whatever your Medigap/Advantage plan leaves you with. In 2025, that deductible is $257.

In real life, people fall through cracks: exams billed under the wrong code, visits scheduled a month too early, or high-risk patients who never learn they qualify at all. I managed to do all three before I finally sat down with my paperwork and a highlighter.

The quick win: if you have diabetes or a family history of glaucoma, assume you might be high risk and confirm it—don’t wait for someone to volunteer it.

- Glaucoma can progress silently for years.

- High-risk status makes regular screening affordable.

- Your doctor won’t always bring it up first.

Apply in 60 seconds: Write down whether you have diabetes, glaucoma in the family, or are African American 50+ or Hispanic 65+—you’ll use this list later with your doctor.

Who counts as “high risk” under Medicare rules (2025, US)

Let’s strip this down to what Medicare actually says, not what friends or receptionists vaguely remember.

Under current rules, Medicare considers you “high risk for glaucoma” if at least one of the following applies to you:

- You have diabetes (Type 1 or Type 2).

- You have a family history of glaucoma (parent, sibling, or sometimes a grandparent, depending on the doctor).

- You’re African American and 50 or older.

- You’re Hispanic/Latino and 65 or older.

If that’s you, Medicare Part B covers a glaucoma screening exam once every 12 months when it’s done by an eye doctor who is legally allowed to perform the test and who bills Medicare correctly.

Notice what this list doesn’t include: high blood pressure, nearsightedness, steroid use, or “just getting older.” All of those can raise your true medical risk of glaucoma, but they don’t automatically qualify you for the special high-risk benefit under Medicare’s rules.

In other words, there are two kinds of “high risk”:

- Medically high risk: many factors your eye doctor thinks about.

- Medicare high risk: the narrow set of criteria that change how the bill is paid.

I spent a full year assuming my “borderline” eye pressure meant I was high risk under Medicare. I wasn’t. My diabetes diagnosis is what unlocked the benefit, not the borderline numbers.

Money Block #1 — 60-second high-risk eligibility checklist

Answer each question with a simple yes/no:

- Has a doctor diagnosed you with diabetes?

- Has any parent, brother, sister, or child been told they have glaucoma?

- Are you African American and 50 or older?

- Are you Hispanic/Latino and 65 or older?

If you answered “yes” to at least one: you likely meet Medicare’s high-risk criteria for a glaucoma screening every 12 months. Bring this list to your next appointment and ask the eye clinic to confirm and note it in your chart, including the exact risk factor they’re using.

Neutral next step: Save this checklist with your insurance card and ask the receptionist to confirm your high-risk status before they book your next “Medicare glaucoma screening” exam.

- At least one of four criteria is enough.

- Plenty of medically risky people don’t qualify under Medicare’s definition.

- Having diabetes or a qualifying family history is often the simplest path.

Apply in 60 seconds: Circle which of the four official criteria you meet and write it on a sticky note for your next eye visit.

How glaucoma screenings work when you’re high risk

A “glaucoma screening” under Medicare isn’t just a quick puff-of-air test in a mall optical shop. It’s a more complete clinical exam designed to spot nerve damage early.

A typical high-risk glaucoma exam under Medicare includes:

- Dilated eye exam: drops to widen the pupil so your optic nerve can be seen.

- Tonometry: measuring eye pressure (with air puff or a blue-light instrument).

- Optic nerve evaluation: the doctor studies the shape and color of the nerve.

- Visual field testing: checking for blind spots using a machine with tiny lights.

Some parts of this are bundled; some may be billed separately as diagnostic tests. That’s where cost confusion starts. A quick “screening” that turns into “we found something, let’s run more tests” can change your bill from one line item to several.

When this happened to me, the tech casually said, “We’ll just add a visual field today.” I nodded… and then spent 20 minutes at home trying to decode the extra line items on my statement.

Show me the nerdy details

Under Medicare, the glaucoma screening benefit is tied to specific procedure codes and requires that the exam be performed or supervised by a legally qualified eye care professional who accepts Medicare. Additional testing, such as optical coherence tomography (OCT) or extra visual field exams, can be billed as diagnostic services when medically necessary. These are usually subject to the same Part B deductible and 20% coinsurance but are not always considered part of the “once every 12 months” screening.

The bottom line: a screening is really a structured, billable bundle of services wrapped around one big question—is your optic nerve quietly dying or not? If you’re high risk, Medicare wants that question answered every year.

What Medicare Part B and Advantage actually pay

Now to the money—and why my first “free” glaucoma visit was anything but.

If you have Original Medicare (Part A & B) and no extra coverage, here’s the basic pattern for glaucoma screening costs in 2025:

- You pay the Part B deductible first: $257 in 2025.

- After that, Medicare usually pays 80% of the approved amount for covered services.

- You pay the remaining 20% coinsurance, unless another policy (like Medigap) helps.

If the exam is billed as a covered glaucoma screening for a high-risk patient, the same 80/20 pattern applies. If the exam is coded as something else—routine vision, refraction, or non-covered testing—you may be on the hook for more.

For Medicare Advantage (Part C) plans, things vary by carrier. Some plans charge a flat copay for specialist visits (for example, $35–$50), others use tiered copays depending on whether you’re at a hospital clinic or private office. Many plans include glaucoma screening in that specialist copay, but extra diagnostic tests may still trigger separate coinsurance.

| Coverage type (2025) | What you usually pay | Notes |

|---|---|---|

| Original Medicare only (Part B) | Part B deductible ($257), then ~20% of approved amount | Assumes provider accepts assignment; amounts vary by region. |

| Medicare + Medigap Plan G | Usually just the Part B deductible, then often $0 | Medigap may cover the 20% coinsurance once deductible is met. |

| Medicare Advantage (Part C) | Specialist copay (often $30–$60), plus coinsurance on extra tests | Check your plan’s Summary of Benefits for eye-care line items. |

Money Block #2 — Quick glaucoma screening fee table (2025)

This table is a starting point, not a quote. Actual billed amounts depend on where you live, how your doctor codes the visit, and whether extra tests are needed. Use it to frame one simple question at check-in: “If this is billed as a Medicare glaucoma screening because I’m high risk, what is my expected out-of-pocket today?”

Neutral next step: Save this table or write down your coverage type and ask the billing desk to confirm your estimated cost before your pupils are dilated.

- Part B: deductible + 20% coinsurance is the default pattern.

- Medigap can erase much of the 20% if you’ve met the deductible.

- Advantage plans swap 20% coinsurance for predictable copays.

Apply in 60 seconds: Write down your plan type (Original + Medigap vs Advantage) and one question for your next visit: “What will I owe today if it’s billed as a high-risk Medicare glaucoma screening?”

7 costly mistakes I sadly learned the hard way

Here’s the part I wish I could mail back to my past self in a sealed envelope. These seven mistakes cost me money, time, and a few months of quiet panic. You get the edited version.

1. Assuming “I’m fine, I can see well” meant I wasn’t high risk

For two years after my diabetes diagnosis, I treated my decent vision as a green light to skip proper eye exams. I could still read road signs; I didn’t notice any halos. That had nothing to do with whether glaucoma was chewing on my optic nerve.

If you have diabetes, a qualifying family history, or you meet the age–race criteria, your vision today is not the deciding factor. The whole point of screening is to see damage before you do.

2. Letting reception book “a regular eye exam” instead of a high-risk screening

At one clinic, the receptionist cheerfully booked me for a “routine eye check” with refraction to update my glasses. The visit was helpful, but it was not billed as a glaucoma screening for a high-risk patient. I walked out with new lenses and no documented high-risk exam on file for Medicare’s purposes.

The tiny script that would have fixed it: “Please book me for a Medicare glaucoma screening exam; I’m high risk because of diabetes/family history/etc.”

3. Going to providers who didn’t clearly accept Medicare assignment

One year, I picked an eye clinic because it was close to my favorite coffee shop. They were “in Medicare,” but they didn’t always accept assignment—that is, they sometimes billed more than the Medicare-approved amount and balanced-billed patients the extra.

My share jumped from a predictable 20% to a confusing soup of line items and “non-covered differences.” If you’re on a tight budget, that surprise hurts as much as the dilation drops.

4. Ignoring the 12-month timing rule

I once booked my “annual glaucoma check” at 11 months because that’s when my schedule opened up. Medicare’s language is closer to once every 12 months, not “once per calendar year.” That one-month eagerness risked pushing part of the visit into a different billing category.

The fix is simple: aim for one full year plus a week or two, especially if your last visit got pushed later in the year.

5. Letting add-on tests pile up without asking about cost

Glaucoma care is layered. Visual fields, OCT scans, optic nerve photos—each may be medically appropriate. But if nobody warns you, a “quick check” can turn into several hundred dollars of line items before your pupils finish shrinking.

One year, an extra OCT scan and a surprise second visual field test added almost $200 to my out-of-pocket because I hadn’t met my deductible yet.

6. Never checking how my Medigap or Advantage plan handles eye-care coinsurance

I used to treat my supplemental coverage like magic. “It’s fine, Medigap pays.” Except not always. Some plans handle diagnostic eye tests differently; some Advantage plans require prior authorization for certain procedures.

Once, a delayed authorization turned a same-day test into a rescheduled, second visit—another copay, another round-trip drive.

7. Letting open enrollment slide while my risk was rising

Glaucoma doesn’t care about open enrollment, but your plan choices do. I stayed in a bare-bones plan while my risk profile changed—diabetes, family history solidified, nerve readings edging toward suspicious.

By the time I started taking my eye risk seriously, I’d missed the best window to switch into a plan with stronger specialty coverage and predictable copays. That mistake stretched across several years of appointments.

- How the visit is booked and coded matters as much as the visit itself.

- Providers’ billing habits directly affect your out-of-pocket cost.

- A 15-minute review during open enrollment can save years of frustration.

Apply in 60 seconds: Pick one of the seven mistakes you’ve made (or nearly made) and write a one-line rule for yourself on a sticky note—for example, “Always say: ‘Book me as a Medicare glaucoma screening; I’m high risk because of X.’”

Money Block: check your out-of-pocket before the visit

Glaucoma talk can feel abstract. Bills are not. This mini-estimator won’t give you an exact quote, but it will anchor your expectations and help you ask sharper questions at the front desk.

Money Block #3 — 60-second out-of-pocket estimator

Fill in three tiny blanks and you’ll have a ballpark number to sanity-check against the clinic’s estimate.

Neutral next step: Bring your estimate to the clinic and say, “This is what I’m expecting to pay under Medicare rules—can you confirm or correct this before we start?”

Is this perfect? No. But it forces one crucial mental habit: eligibility first, quotes second. You’ll save 20–30 minutes of back-and-forth and avoid surprise bills that arrive weeks after your pupils return to normal.

How diabetes, family history, and ethnicity shape your real risk

Medicare’s checklist is short. Reality isn’t. Let’s walk through why each of the high-risk factors matters and what it means for your long-term vision.

Diabetes: People with diabetes are more likely to develop several eye conditions, including glaucoma, diabetic retinopathy, and cataracts that sometimes end in surgery. Diabetes affects blood flow to the optic nerve and can increase eye pressure. It also tends to come with other vascular issues—hypertension, cholesterol—that quietly stack risk.

Family history: If a parent or sibling has glaucoma, your own odds rise significantly. Families not only share genes but also shared health habits and barriers to care. In my case, an uncle’s “mysterious” vision loss in his 70s turned out to be untreated glaucoma that was never fully explained to the rest of us.

Ethnicity and age: Glaucoma hits some groups harder. African Americans have a higher risk of developing glaucoma and of going blind from it, often at younger ages. Hispanics and Latinos see risk climb sharply after 60–65.

Medicare doesn’t list every nuance in its high-risk policy, but its criteria mirror what eye-health organizations have been warning about for years.

Show me the nerdy details

Research over the past decade has repeatedly shown that glaucoma prevalence and severity vary by ethnicity, age, and co-existing conditions. African Americans often experience earlier onset and more aggressive disease courses. Hispanics and Latinos see risk surge after age 60, particularly for open-angle glaucoma. Normal-tension glaucoma after 60, in which optic-nerve damage happens despite “normal” pressure readings, is another pattern doctors watch closely. Medicare’s high-risk categories are a simplified reflection of this research, not a complete map of individual risk.

Here’s the practical takeaway: even if you don’t meet Medicare’s formal high-risk definition, these medical factors still warrant serious eye care. The difference is financial, not moral. You may still need regular glaucoma checks and dilated eye exams; you may just have to budget differently or rely more heavily on what your Advantage or Medigap plan covers.

- Diabetes, family history, and ethnicity influence both risk and coverage.

- Some medically risky people don’t meet the Medicare high-risk definition.

- Your true risk is a medical conversation; coverage is an insurance conversation.

Apply in 60 seconds: Write down which medical risk factors you have beyond Medicare’s official list—high blood pressure, long-term steroids, past eye trauma—and ask your eye doctor how they change your exam schedule.

What to ask your eye doctor in 15 minutes or less

Most eye visits feel rushed. The doctor is behind; your pupils are already dilating; your brain is juggling parking times and dinner plans. You need a tiny, sharp checklist—not a script you’ll never use.

Here’s the five-question mini-interview I settled on after a few chaotic visits:

- “Based on my history, do I meet Medicare’s high-risk criteria for glaucoma?”

- “Will today’s visit be billed as a Medicare glaucoma screening or something else?”

- “Are you planning any extra tests besides the basic screening? About how much do they usually cost under my coverage?”

- “Has my optic nerve or visual field changed compared with last year?”

- “What’s the one thing you want me to watch for at home between now and next year?”

Short Story: On one visit, I walked in with 20 printed questions. I got through… two. The doctor was kind but clearly overwhelmed, and I left with my list barely touched. The next year, I tried just three questions, all written in big letters on a half-sheet I kept in my hand. The entire energy of the visit shifted. The doctor answered each clearly, even drew a rough sketch of my optic nerve, and I walked out calmer. That was when I learned that fewer, sharper questions beat long, anxious lists. My notes from that visit are the ones I still check when I’m worried late at night.

Money Block #4 — Quote-prep list before you compare coverage

Before you call a new clinic or compare Medicare Advantage plans, gather:

- Your exact diagnoses (diabetes type, any prior “glaucoma suspect” notes).

- Your last glaucoma exam date and clinic name.

- Whether you’ve met your Part B deductible this year.

- The names of any eye drops or past glaucoma treatments.

An annual eye exam checklist for seniors can keep all of this on a single page you bring to every visit.

Neutral next step: Keep this list with your Medicare card and bring it whenever you shop for new coverage or visit a new eye clinic, so quotes reflect your actual risk.

Glaucoma on Medicare if you live outside big cities

If you live in a big metro area, the hardest part of glaucoma care is choosing among too many clinics. Outside cities, it can feel like the opposite: one overbooked provider within an hour’s drive, plus snow.

The good news is that Medicare’s rules don’t change by ZIP code. If you’re high risk, you’re still entitled to a glaucoma screening every 12 months under Part B. The challenge is logistics: getting to a provider who can actually perform the necessary tests and bill correctly.

Practical moves if you’re rural or semi-rural:

- Ask if your local optometrist does full glaucoma screening and bills Medicare, or if they refer out.

- Check whether any regional health systems run glaucoma or diabetic eye-clinic days with mobile equipment.

- If you use a Medicare Advantage plan, confirm network coverage for the nearest eye clinic that does glaucoma testing, not just routine exams.

Many people in small towns quietly space out eye exams to “every few years” because the drive is annoying. I’ve done the same with other specialties. But glaucoma doesn’t care about your mileage; it cares about your optic nerve.

If the trip is long, stack tasks: get labs drawn, see another specialist, or run errands near the clinic. That way your “glaucoma day” feels like a multi-purpose health reset, not just a chore.

- Your high-risk benefit doesn’t shrink just because you live far away.

- Regional clinics and health systems may cluster eye-care days—ask.

- Bundling appointments can turn one long trip into a high-yield health day.

Apply in 60 seconds: Look up the nearest eye clinic that offers glaucoma testing, note the mileage, and sketch a “health errand day” that would make the trip feel worthwhile.

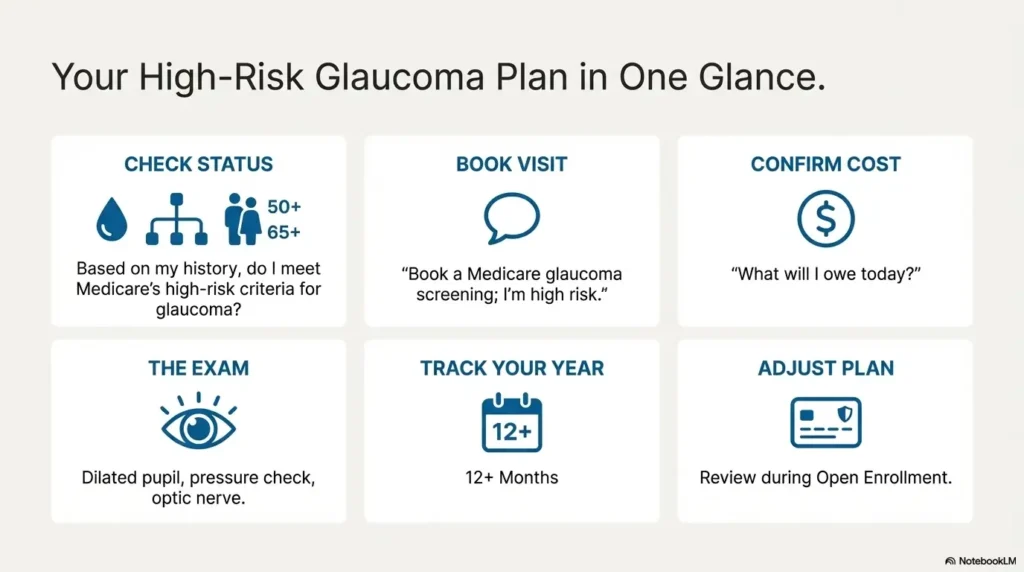

Infographic: high-risk glaucoma on Medicare in one glance

High-risk glaucoma on Medicare in 6 boxes

A quick visual map from “Do I qualify?” to “What do I pay?” and “What do I ask?”

1. Check high-risk status

- Diabetes?

- Family history?

- African American 50+?

- Hispanic/Latino 65+?

2. Book the right visit

Say the magic words: “Medicare glaucoma screening; I’m high risk because of X.”

3. Confirm costs

Ask: “What do I owe today under my plan if it’s billed as a screening?”

4. Understand the exam

Dilated exam + pressure + nerve check; extra tests may add cost.

5. Track your year

Note the exact date; aim for 12+ months before your next screening.

6. Adjust your plan

Use open enrollment to pick coverage that fits your ongoing glaucoma risk.

FAQ

Here are straight answers to common questions I hear from friends, readers, and the worried people in waiting rooms who quietly ask, “Do you understand this stuff?”

1. How often will Medicare pay for a glaucoma screening if I’m high risk?

Medicare Part B generally covers one glaucoma screening exam every 12 months for people who meet the high-risk criteria—diabetes, qualifying family history, African American age 50+ or Hispanic/Latino age 65+. The clock is based on the date of the exam, not the calendar year. A good habit is to schedule your next visit a little more than a year later—say 12–13 months—to avoid any timing disputes.

60-second action: Look up the date of your last dilated glaucoma exam and write it on the inside cover of your Medicare card holder or in your phone’s calendar with a reminder set for 11 months later.

2. What if I’m high risk medically but don’t fit Medicare’s narrow definition?

You can absolutely still need careful glaucoma monitoring even if Medicare doesn’t label you as “high risk” for the special screening benefit. Conditions like high blood pressure, strong short-sightedness, or long-term steroid use can increase your true medical risk. In those cases, your eye doctor may still order glaucoma-related tests; they’ll just be billed under different medical codes. You’ll likely follow the usual Part B pattern: deductible, then 20% coinsurance, or your Advantage plan’s copay scheme.

60-second action: Ask your eye doctor, “Do you consider me medically high risk for glaucoma, even if Medicare doesn’t? If yes, how often do you want to see me?” Then write the answer down.

3. Does Medicare cover eye drops or surgery if I’m diagnosed with glaucoma?

Once glaucoma is actually diagnosed, you move out of the “screening” world and into treatment. Medicare Part B may cover certain office-based treatments and surgeries (like laser procedures and cataract surgery) when medically necessary, following the usual deductible and coinsurance rules. Glaucoma eye drops are usually handled under Part D (drug coverage) or your Medicare Advantage plan’s drug benefit. Coverage levels differ a lot between plans, which is why people with glaucoma often pay close attention to Part D formularies during open enrollment.

60-second action: If you’re already on glaucoma drops, take a photo of the bottle and ask your plan’s drug helpline or pharmacist what your tier, copay, and any cheaper equivalent options are.

4. What should I do if I think my glaucoma screening was billed incorrectly?

First, request an itemized bill from the clinic and compare it with your Medicare Summary Notice or Advantage Explanation of Benefits. Check whether the visit is described as a glaucoma screening for a high-risk patient or as a generic office visit or refraction. If something seems off, call the clinic’s billing department and politely ask them to walk you through each line. Sometimes it’s just confusing wording; sometimes a code really is wrong and can be corrected.

60-second action: Circle any line item you don’t recognize on your bill and call the number on the statement with one question ready: “Can you explain what this code means and why it was needed?”

5. Can I appeal if Medicare or my plan denies part of the glaucoma exam?

Yes. If a service you thought would be covered is denied, you can usually file an appeal. For Original Medicare, you’d follow the instructions on your Medicare Summary Notice. For Medicare Advantage or Part D, you follow your plan’s appeal steps. Your eye clinic can sometimes help by clarifying medical necessity or sending supporting notes. Appeals take time and patience, but they’re worth considering if a significant bill lands in your lap unexpectedly.

60-second action: Keep all paperwork from your visit in one folder and highlight any “denied” line; if the amount is large, call the clinic and ask whether they believe an appeal makes sense before you start.

6. I’m on Medicare but live part of the year outside the US. What happens then?

Medicare generally doesn’t cover care outside the United States, with only narrow exceptions. If you spend months abroad and delay glaucoma screening until you’re overseas, you may end up paying fully out-of-pocket in that country. The safer move—if you know you’re high risk—is to time your annual glaucoma exam for when you’re back in the US and fully within your Medicare coverage. That way, your most important nerve-check happens under a familiar billing system.

60-second action: If you’re a “snowbird” or frequent traveler, pick one month each year when you’re reliably in the US and mark it as your standing glaucoma exam month on your calendar.

Conclusion: your next step in the next 15 minutes

We started with a quiet fear: What if I’m losing vision and don’t know it? Along the way, we translated Medicare’s high-risk rules into normal language, walked through real cost patterns, and laid out the seven mistakes that drained my time, money, and courage more than once.

Here’s the honest truth: glaucoma will never feel urgent on a Tuesday morning. The letters on the page still look sharp; the world still shows up in full color. It’s easy to file small vision changes under “just getting older” instead of asking whether a serious eye disease is starting to take root.

Here’s the honest truth: glaucoma will never feel urgent on a Tuesday morning. The letters on the page still look sharp; the world still shows up in full color. But the nerve damage that steals sight rarely announces itself early. That’s why Medicare built a specific high-risk door for people with diabetes, family history, and certain age–ethnicity combinations—and why it’s worth the small administrative hassle to walk through it.

You don’t need to “fix” everything today. All you need is one clear next step.

- If you haven’t had a dilated glaucoma exam in over a year, call your eye clinic and say: “I’m high risk for glaucoma because of X. I’d like to schedule a Medicare glaucoma screening exam.”

- If you’re unsure of your status, bring the four-question checklist from earlier and ask your doctor to confirm it in writing in your chart.

- If your bills have been confusing, use the out-of-pocket estimator and table to frame one calm conversation with the billing desk.

- Know whether you meet the high-risk definition.

- Book the right kind of visit at the right time.

- Ask one or two sharp money questions before you sit in the chair.

Apply in 60 seconds: Set a 15-minute timer, grab your Medicare card and calendar, and either schedule your next glaucoma screening or write down the one question you’ll bring to your current eye doctor about your high-risk status.

Last reviewed: 2025-12; sources included official Medicare publications and major US eye-health organizations. Many of those same organizations outline the major age-related eye diseases after 60 that often travel alongside glaucoma. Coverage details and dollar amounts can change; always confirm current rules with Medicare, your plan, or your eye clinic before making decisions.