The Eye Exam “Jump-Scare”:

Understanding Your Medicare Bill

You leave the eye clinic feeling fine—then the statement lands with two charges for one “eye exam,” like a jump-scare you didn’t audition for. That surprise usually isn’t fraud. It’s a category mismatch: a Medicare eye exam can quietly contain two different services, and only one lives in the “covered” lane.

The Key Definition: Refraction is the “Which is better—1 or 2?” testing used to write a glasses or contacts prescription. Under Original Medicare (Part B), routine refraction is typically self-pay, even when the medical evaluation is billed to Medicare.

Keep guessing and you’ll keep getting cornered at checkout—blurred from dilation, rushed, and signing forms you didn’t have time to read (hello, ABN vibes).

This guide gives you a calm, repeatable system: one scheduling sentence, six pre-visit questions, and a simple way to spot where the extra line item is hiding on an itemized bill.

Just predictable costs and clean receipts.

Table of Contents

Refraction vs. medical exam: the two-lane visit Medicare treats differently

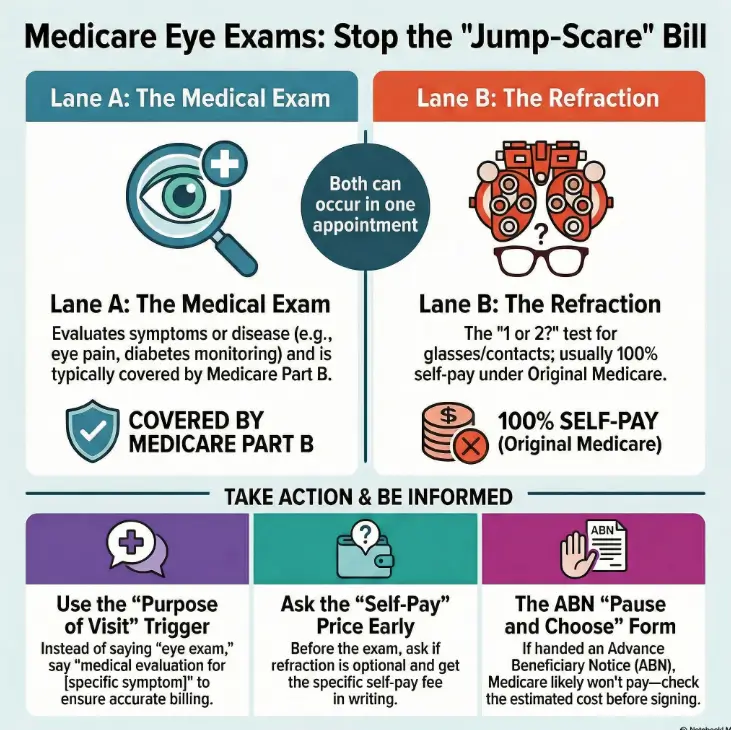

Here’s the core truth that removes most confusion: Medicare treats many eye visits as one of two “lanes.” Lane A is a medical evaluation for a problem (symptoms, disease monitoring). Lane B is refraction—the “which is better, 1 or 2?” sequence used to write a glasses/contacts prescription. Medicare’s public coverage pages are blunt about it: routine eye refractions for eyeglasses or contacts aren’t covered under Original Medicare, and people often pay the full amount for that portion.

And yes, both lanes can happen in the same appointment. That’s where surprise bills are born: not because you did something wrong, but because the visit quietly shifted from “medical problem” to “also, let’s update your glasses.”

- Often billed to Part B when medically necessary

- Your share may include deductible/coinsurance

- Typically not covered by Original Medicare

- Often self-pay, billed separately

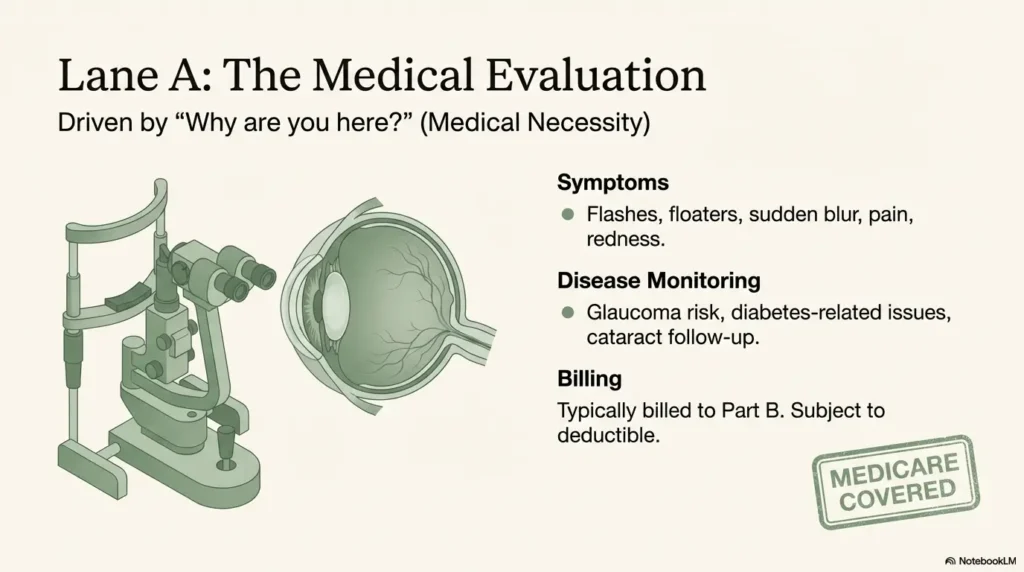

Medical exam lane: symptom/problem evaluation (why coverage may apply)

If you’re there because of a symptom (pain, sudden blur, flashes, redness, swelling), or because you’re being monitored for a condition (such as diabetes-related eye issues, glaucoma risk, cataract follow-up, or hypertensive retinopathy), the visit is commonly framed as medical evaluation. That framing matters because Medicare coverage tends to follow “medical necessity” rather than “I want new glasses.”

Refraction lane: the glasses/contacts prescription test (why you usually pay 100%)

Refraction is the part where they refine lens power: better 1 or better 2. It can feel medically “serious” because it’s done by professionals with fancy equipment, but Medicare’s line is about purpose. If the purpose is writing a corrective lens prescription, Original Medicare generally doesn’t cover it.

One appointment, two outcomes: how both lanes happen on the same day

Picture the common scenario: you booked because “my vision has been off lately,” and during the exam the clinician says, “We can also update your glasses while you’re here.” That sounds helpful (and it can be). But it’s also the moment Lane B quietly appears. The fix isn’t arguing; it’s choosing intentionally: “Yes, and tell me the refraction self-pay fee first,” or “Not today—I’m here for the medical evaluation.”

- Lane A = medical evaluation for a problem

- Lane B = refraction for glasses/contacts

- You can accept Lane A and decline Lane B

Apply in 60 seconds: Write down your visit purpose in one sentence before you call to schedule.

Coverage trigger word: the “purpose of visit” detail that flips the billing story

If you only remember one thing from this article, make it this: the purpose of the visit is the coverage trigger. Not the building. Not the fancy machines. Not how long you were there. Purpose.

Curiosity gap: why “my vision changed” can still be treated as routine

“My vision changed” is a true statement—but it’s also vague. For scheduling staff (who are not mind-readers), it can sound like, “I need new glasses.” That pushes you straight toward refraction. If you mean something else—new floaters, distortion, sudden blur, a painful red eye—you need to say the symptom out loud.

The scheduling phrase that protects you: “medical evaluation for ___ symptoms”

Try this: “I need a medical evaluation for [specific symptom].” Examples:

- “Medical evaluation for new flashes and floaters.”

- “Medical evaluation for eye pain and redness.”

- “Medical evaluation for sudden blurry vision in my right eye.”

This does two things: it helps the clinic schedule appropriately, and it creates a clear record of intent. You’re not asking them to “make it covered.” You’re being accurate. Accuracy is the cheapest form of insurance.

What to document (date, name, quote, optional vs required services)

Write down: date/time, the staff member’s name (or first name), what they said about refraction being optional, and the self-pay quote. If you’re a caregiver, this is where you become the hero: a small note today can prevent an exhausting phone-tree tomorrow. (If you like checklists, you can use a printable symptom diary for seniors to keep dates, symptoms, and quotes in one place.)

- Yes — You have a symptom, diagnosis, or monitoring need (medical lane likely applies)

- No — You only want a new glasses/contacts prescription (refraction lane likely applies)

- Mixed — You want both today (expect two line items unless your plan says otherwise)

Neutral next step: Call the office and ask, “Can refraction be declined if I’m here for the medical evaluation?”

Test stack reality: what “a thorough eye exam” usually includes—and what counts as refraction

Clinics often run a “test stack”—a set of standard steps that make visits efficient and safe. The problem is that the stack can feel like one unified service, even when billing splits it into covered and non-covered parts. You’re not being picky by asking what each test is for. You’re being adult about money.

Visual acuity (eye chart) vs refraction (the “1 or 2?” sequence)

The eye chart is a visual acuity check—how well you see at distance (and sometimes near). Refraction is the prescription refinement. They’re related, but they’re not the same thing. If someone says, “We’ll just do the quick vision test,” you can gently ask, “Is that the eye chart only, or does that include refraction for a glasses prescription?”

Slit lamp + retinal exam: why “medical-looking” tests can still appear in routine workflows

A slit lamp exam and retina checks can show up in both lanes. A clinic can perform careful health checks during a routine vision visit (good medicine), while Medicare still considers the visit routine if the primary purpose is a prescription. This is where patients feel betrayed—because “thorough” feels like “covered.” It isn’t always.

Dilation: when it’s common, when it’s medically driven, what to ask

Dilation is often used to get a better look at the back of the eye. Sometimes it’s standard for a comprehensive evaluation; sometimes it’s driven by symptoms or disease risk. Ask two practical questions: “Do I need dilation today?” and “Is it part of the medical evaluation or part of the routine vision exam process here?” The point isn’t to debate—it’s to understand. (If you’re wondering about timing and frequency, see how often seniors should get dilated eye exams.)

Prescription decoder: what you’re actually buying when you pay for refraction

When you pay for refraction, you’re buying a specific output: a prescription. Once you see it as an output, it becomes easier to decide whether you want it today, from this clinic, at this price.

SPH / CYL / Axis: what these numbers do (and don’t) mean

SPH is the basic lens power for nearsightedness or farsightedness. CYL and Axis relate to astigmatism—how the lens corrects an uneven curve. These numbers don’t tell you “how bad your eyes are” as a person. They tell you what lenses to make so your vision is clear.

ADD / Prism / PD: when they appear and why costs can rise

ADD is common in multifocal prescriptions for reading. Prism can be used for certain alignment issues. PD (pupillary distance) affects how lenses are centered. Costs often rise not because the prescription is “fancy,” but because it leads to premium lens options (progressives, specialized measurements, add-ons). That’s a shopping decision as much as a medical one.

Open loop: the one line item that often signals “this was refraction”

If your receipt or itemized statement includes a line that clearly refers to refraction or “glasses prescription,” that’s usually the Lane B charge. If the wording is vague, ask: “Which line is for the refraction?” Make them point to it. Calmly. Like you’re choosing a seat on an airplane.

Bill anatomy: how one visit becomes multiple charges (and where surprises hide)

Let’s demystify the bill without pretending there’s one universal format. Most surprise bills happen for one of three reasons:

- Two services happened (medical evaluation + refraction) and you only expected one.

- The location changed the bill (hospital outpatient departments can add facility fees).

- Consent happened in a hurry (you signed something or verbally agreed without a price).

Professional fee vs facility fee: why “hospital outpatient” can cost more

If your eye visit is billed through a hospital outpatient department, you may see a professional charge (for the clinician) and a facility charge (for the setting). This isn’t unique to eye care—it’s a general billing structure that surprises people because it feels like you went to “a clinic,” not “a hospital.” If you’re cost-sensitive, ask at scheduling: “Is this billed as hospital outpatient?” That one question can change your expectations.

Here’s what no one tells you… “thorough” ≠ “covered”

Thorough care is good. Covered care is a separate concept. A clinic can do thorough work during a routine vision visit. Medicare can still say, “That refraction for glasses isn’t covered.” This is not a moral judgment. It’s a category decision.

Curiosity gap: why the same test can land in different billing buckets depending on intent

Some tests are used in both lanes. The billing bucket often follows the documented purpose and the overall structure of the visit. That’s why clarity at scheduling and check-in is so powerful: you’re not changing medicine—you’re reducing ambiguity.

| Year | Line item | Quoted range (from clinic) | Notes |

|---|---|---|---|

| 2026 | Refraction (glasses/contacts prescription) | $____ to $____ | Ask if optional; ask if billed separately |

| 2026 | Medical evaluation (symptom/problem) | $____ to $____ | Ask if billed as hospital outpatient (facility fee?) |

Neutral next step: Put this table next to your phone before you call. Fill it in while they’re talking.

Pre-visit script: 6 questions to ask before you consent to refraction charges

This section is the money. Not because it’s aggressive—because it’s early. The best time to prevent a surprise bill is before you’re in the chair with a technician waiting and your brain trying to be polite.

“Will refraction be performed today? What’s the self-pay price?”

You’re not asking for a favor. You’re asking for a number. If they can’t give an exact price, ask for a range and ask who can confirm it (billing desk, office manager). Write down the answer.

“Is refraction optional if I’m here for a medical problem?”

This is the fork in the road. If it’s optional, you can say: “Let’s focus on the medical evaluation today. I’ll decide about refraction after we talk.” If it’s required for their workflow, ask why—and ask what portion is self-pay.

“Will you bill Medicare for the medical exam and bill refraction separately?”

Many offices do exactly this. The important part is that you hear it stated plainly before the visit, not discovered at checkout like an unwanted plot twist.

“Can you note ‘decline refraction unless medically necessary’ in my chart?”

Charts are where intentions go to live. A note like this can prevent the automatic “and now we do refraction” routine. If you’re nervous saying it, try: “I’m on a strict budget and want to avoid non-covered charges unless we truly need them today.”

Let’s be honest… checkout is where clarity goes to die (so we ask early)

Checkout desks are busy. People behind you are sighing. You’re thinking about dilation blur and where you parked. That’s not a good moment to negotiate consent. Do it earlier—calmly—when everyone still has time.

Short Story: The two-minute phone call that saved a three-hour mess

Imagine you’re scheduling for your dad. He says, “Just book the eye exam.” You call the clinic, and the scheduler offers the next slot. Right as you’re about to say yes, you ask one extra question: “Will refraction be done, and what’s the self-pay fee if Medicare doesn’t cover it?” There’s a pause.

Then: “Oh—yes, we usually do that. It’s billed separately.” You ask if it’s optional because he’s coming for new flashes in one eye. Another pause. “In that case, we can skip refraction today and focus on the medical evaluation.”

Two minutes later, you’ve turned a fuzzy appointment into a clean plan. No confrontation. No guilt. Just a visit that matches the real goal. When you’re the person who handles the phone calls, that’s what winning looks like: quiet, precise, and done before the day gets chaotic.

- Ask if refraction is planned

- Ask if it’s optional

- Ask the self-pay price and write it down

Apply in 60 seconds: Copy the six questions into a note on your phone titled “Eye Visit Script.”

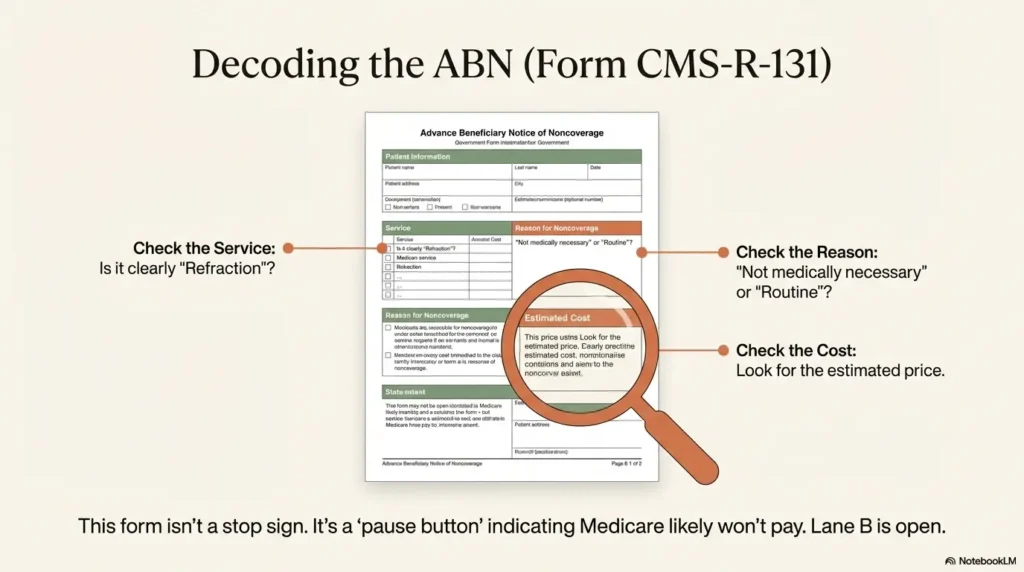

ABN reality check: what it is, when it matters, and what to do if you’re handed one

Sometimes, the office hands you a form with serious vibes: the Advance Beneficiary Notice of Noncoverage (ABN). This is a Medicare Fee-for-Service (Original Medicare) form used when a provider believes Medicare may not pay for a specific item or service in a specific situation. The official form name is often listed as CMS-R-131.

What an ABN is (and why providers use it when denial is expected)

An ABN is meant to help you make an informed choice: get the service and accept potential financial responsibility, or decline it. It’s not automatically “bad.” It’s a moment where the system says, “Pause and choose.”

What to ask before signing: item/service name, reason, estimated cost

- What exactly is the service? (“Refraction for glasses prescription” should be stated clearly.)

- Why do you expect Medicare won’t pay? (Non-covered vs not medically necessary.)

- What is the estimated cost? (A number, not a shrug.)

Open loop: the small checkbox choice that changes who pays

ABNs often include options about whether the provider should submit a claim to Medicare. That choice can affect what paperwork exists later. If you’re unsure, slow down. Ask for a moment to read. Ask them to explain each option in plain language. You’re allowed to take your time—your wallet will remember whether you did.

Show me the nerdy details

In Medicare terminology, the ABN is used to shift potential financial liability to the beneficiary when coverage is expected to be denied in a specific case. It’s designed for Original Medicare (Fee-for-Service). Medicare Advantage plans often use different processes and forms, so the presence—or absence—of an ABN doesn’t always mean the same thing across plan types.

Who this is for / not for

Let’s get honest about fit, because nothing wastes time like reading the wrong rulebook.

For you if: Original Medicare + symptoms/monitoring + cost anxiety

If you’re on Original Medicare and you’re coming in for symptoms or disease monitoring, this guide helps you keep the medical lane clean while choosing (or skipping) refraction intentionally. (If your risk comes from genetics or family patterns, you may also want to note any family history of eye disease when you schedule.)

Not for you if: You only need plan-specific vision benefits (Part C varies)

If you’re on Medicare Advantage, routine vision benefits can vary by plan, network rules, and prior authorization. The “two-lane” idea still helps, but the coverage details are plan-specific.

Not for you if: You need legal advice for a dispute (use the escalation checklist instead)

If you’re already deep in a dispute and need legal strategy, this article won’t replace professional advice. What it will give you is a clean escalation sequence and documentation habits.

- You have symptoms or a diagnosis

- You want to minimize non-covered costs

- You can update glasses later

- You want a prescription today

- You’re comfortable with a separate refraction fee

- You have the self-pay price in writing

Neutral next step: Pick one lane as your default and say it at check-in.

Common mistakes: the phrases and assumptions that cause surprise bills

Surprise bills aren’t usually caused by evil. They’re caused by ambiguous language. Here are the miscommunications that show up again and again.

Mistake #1: Saying “annual eye exam” when you mean “medical evaluation”

“Annual eye exam” sounds routine. Routine sounds like refraction. If you have symptoms, say symptoms. If you have a diagnosed condition being monitored, name it. This isn’t drama; it’s clarity.

Mistake #2: Mixing goals (“check my symptoms + I want new glasses”) without separating them

You can absolutely do both. But when you mix them without separating, the office may default to the full routine workflow plus the medical work. Separate them out loud: “Today I’m here for the medical issue. If time allows, we can discuss refraction pricing before we do it.”

Mistake #3: Not asking the refraction self-pay price upfront

If you don’t ask, you often won’t be told until checkout. Not because anyone is hiding it—because it’s “normal” in their world. You’re allowed to make it normal in your world to ask.

Here’s what no one tells you… clarity is a scheduling skill, not a medical skill

You’re not failing at healthcare. You’re learning a tiny administrative skill that protects your money. It’s like learning where the light switches are in a hotel room—awkward the first time, easy forever after.

- Replace “eye exam” with “medical evaluation for ___” when symptoms exist

- Separate medical goals from glasses goals

- Ask for the refraction price before it happens

Apply in 60 seconds: Practice your one-sentence purpose out loud before the appointment.

Don’t do this: 7 moves that practically guarantee you’ll pay more than expected

This is the “loss prevention” list. No shame—most people learn these the hard way. You don’t have to.

- Don’t accept “we’ll see after” answers when asking about price. Get a range, and ask who can confirm it.

- Don’t assume Medicare Advantage = Original Medicare. Different plan, different rules, different networks.

- Don’t sign forms you haven’t read (especially when you’re dilated and just want to leave).

- Don’t combine a prescription update with a symptom visit unless you’re comfortable with two line items.

- Don’t skip the itemized statement if you’re surprised—vague receipts hide the real story.

- Don’t forget the setting: hospital outpatient billing can add facility fees.

- Don’t rely on memory. Write down the quote and the “optional vs required” answer.

Inputs (max 3): Refraction fee ($___) + Your expected share of covered services ($___) + Any facility fee estimate ($___)

Output: Estimated out-of-pocket today = $___

Neutral next step: Ask the office which of these three numbers they can confirm before you arrive.

When to seek help (medical + billing)

Two kinds of urgency matter here: medical urgency (don’t wait) and billing urgency (don’t ignore). They’re different muscles.

Urgent symptoms (don’t wait): sudden vision loss, severe pain, flashes/curtain, trauma

If something feels truly wrong—sudden vision loss, severe pain, flashes/floaters with a curtain-like shadow, eye injury—prioritize care. Billing can be handled later. Your eyes are not a spreadsheet cell you can “undo.”

Billing escalation path: itemized bill → provider billing office → Medicare general help line

If you’re surprised by charges:

- Ask for an itemized statement with clear descriptions.

- Call the billing office and ask which line represents refraction and whether it was optional.

- If you’re on Original Medicare and you’re confused about coverage categories, call 1-800-MEDICARE for general guidance.

If eligible screenings apply: diabetes eye exams + glaucoma screenings (coverage is specific)

Medicare does cover certain eye-related services in specific situations (for example, certain screenings and exams tied to conditions or risk categories). The key word again is specific. If you qualify, it can be worth asking the office: “Is this being billed as a covered screening/exam, or is this a routine refraction visit?” If you’re trying to estimate what “covered” could still mean for your wallet, you may also want to skim Medicare diabetic eye exam cost and Medicare glaucoma screening for diabetics as quick context before you call.

FAQ

Does Medicare cover refraction for eyeglasses?

Under Original Medicare, routine refraction for eyeglasses or contact lenses is generally not covered. Many clinics bill it as a separate self-pay service. If you have other coverage (a vision plan or a Medicare Advantage plan), benefits may differ.

Why was I charged for refraction during a “covered” eye visit?

Because a single appointment can include both a medical evaluation (potentially covered) and a refraction (often not covered). If refraction was performed to write a glasses prescription, it may appear as its own line item even when the medical portion is billed to Medicare.

Is the eye chart test the same thing as refraction?

No. The eye chart checks visual acuity (how well you see). Refraction is the prescription refinement process (“1 or 2?”). They can happen together, but they aren’t the same service.

Can I refuse refraction and still get checked for eye disease?

Often, yes—especially if your visit is for symptoms or disease monitoring. Ask the office: “Is refraction optional today?” If they say it’s required, ask what clinical reason requires it for your situation.

What is an ABN, and should I sign it?

An ABN is a notice used in Original Medicare settings when a provider believes Medicare may not pay for a service in a specific situation. Don’t sign in a hurry. Ask what service it covers, why Medicare may deny it, and the estimated cost. If you don’t understand, pause and ask for an explanation in plain language.

Do Medicare Advantage plans cover routine vision and refraction?

Many Medicare Advantage plans include some vision benefits, but the details vary by plan, network, and rules. Treat the “two-lane” model as still true, then confirm coverage with your plan documents or plan customer service.

How do I avoid paying twice if I also have a vision plan?

Separate your goals. Use the medical visit for symptoms or monitoring, and use the vision benefit for refraction/prescription when appropriate. Ask both the clinic and your vision plan how coordination works before you schedule.

Next step: one concrete action (copy/paste message)

This is your 15-minute win. Send this message (or say it on the phone) before the appointment. You’re not being difficult. You’re being clear.

Hi—before my visit, can you confirm whether refraction (glasses/contacts prescription) will be performed, the self-pay cost if Medicare doesn’t cover it, and whether it’s billed separately from the medical exam? If refraction is optional, please note whether I can decline it and still complete the medical evaluation.

Neutral next step: Paste this into your patient portal message or text it to the caregiver who schedules for you.

Conclusion

Remember the hook—the bill that arrives like a jump-scare? The quiet antidote is not more stress. It’s one clean decision made early. When you treat an appointment as a “two-lane” visit, you stop being surprised by the system’s categories. You ask the refraction question. You get the price. You decide yes or no. And suddenly, the checkout desk becomes boring again—which is exactly what you want.

If you have 15 minutes today, do this: open your notes app, paste the script, and add one line at the top—your purpose of visit. Then send the message. Future-you will thank present-you with a deep, quiet sigh of relief.

Last reviewed: 2026-01-14