The Hidden Math of Medicare Cataract Surgery in 2026

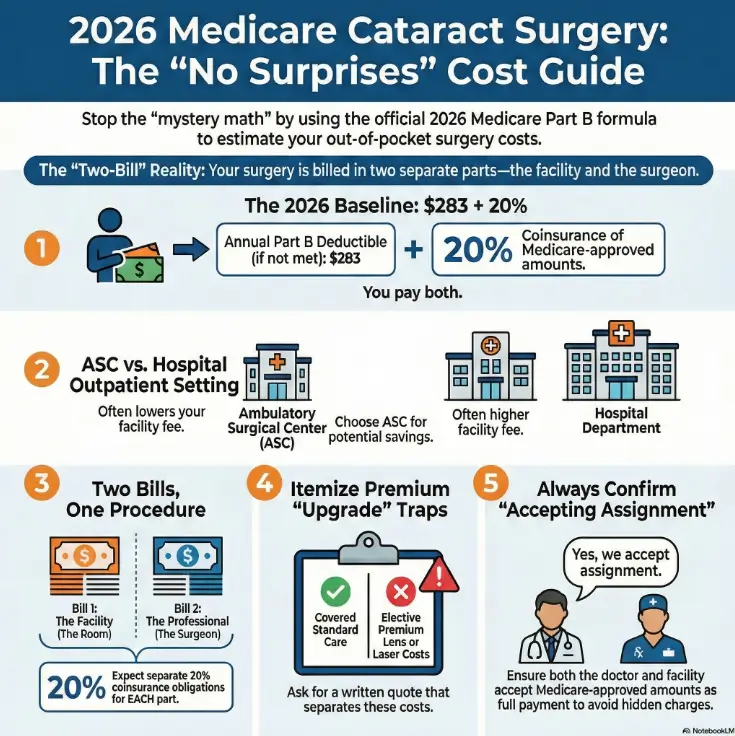

The number most cataract surgery quotes “forget” in 2026 is $283—and it’s usually followed by a second envelope you didn’t budget for. That’s the quiet way “Medicare covers it” turns into mystery math.

If you’re on Original Medicare Part B, the stress rarely comes from the procedure. It comes from scattered pricing: an ASC vs. hospital outpatient setting switch, a quote based on the wrong number, and two separate bills that arrive weeks apart.

The 2026 Cost Mindset

- 2026 Part B Deductible ($283)

- 20% Coinsurance Baseline

- Medicare-Approved Amounts Only

The Two-Bucket Checklist

- Facility Fee: ASC vs. HOPD

- Surgeon Fee: Professional Services

- Prevents the “Sequel Bill”

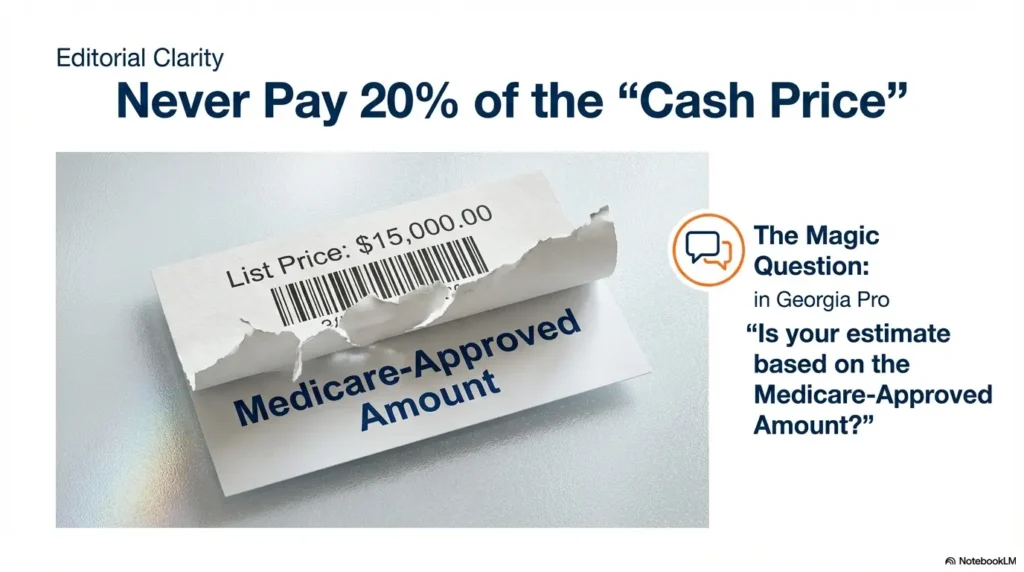

Medicare-approved amount: the payment amount Medicare recognizes for a service in a specific setting. Your 20% coinsurance is typically calculated from this figure—not the clinic’s sticker price or a cash bundle.

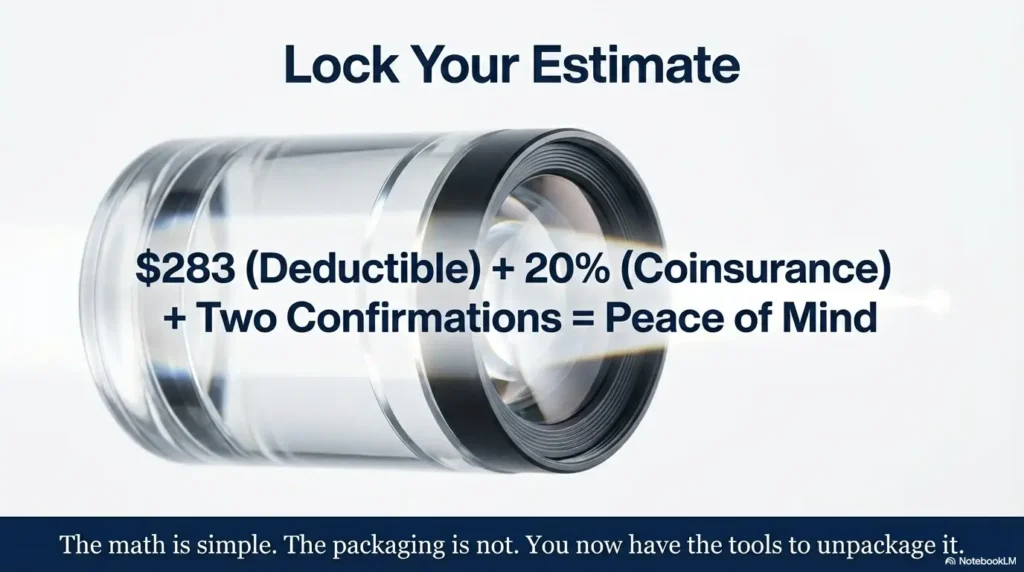

No fog. Two confirmations. Numbers you can actually trust.

Table of Contents

Calculator first: your 2026 Medicare cataract surgery baseline (Deductible + 20%)

Let’s start with the unglamorous truth that makes everything simpler: with Original Medicare Part B, cataract surgery costs are usually built from two pieces— your annual Part B deductible and 20% coinsurance of the Medicare-approved amount (after the deductible is satisfied).

CMS announced the 2026 Part B deductible is $283. That’s the number people forget to include when they’re comparing quotes. I’ve seen a “great deal” turn into a stressful surprise because the estimate quietly assumed the deductible was already met. (It wasn’t.)

- Deductible is annual (calendar-year)

- Coinsurance is a percentage of the Medicare-approved amount (not the “list price”)

- Facility and surgeon can each have their own approved amount

Apply in 60 seconds: Write “$283 + 20%” at the top of your notes before any phone calls.

Mini calculator: deductible + coinsurance (quick estimate)

This is a math helper, not a promise of your final bill. Use it to sanity-check quotes and spot missing pieces.

Show me the nerdy details

This calculator intentionally uses a single “total approved amount” input because many people don’t get facility and professional amounts on the first call. Once you have both, you can run it twice (facility-only and surgeon-only) and add the results. The logic is simple: deductible applies once per calendar year (if not met), then coinsurance is the stated percentage of the approved amounts.

One more grounding detail, because it matters emotionally: you are not “bad at Medicare.” Medicare cost-sharing feels confusing because the same surgery can show up as multiple line items, multiple bills, and multiple mailing dates. The math is simple. The packaging is not.

The 20% is of what, exactly? (approved amount vs “clinic price”)

The 20% coinsurance is tied to the Medicare-approved amount—the amount Medicare recognizes for that service in that setting, not the provider’s sticker price. When a clinic quotes a “cash” number, that can be real, but it’s a different universe than “approved amount.” When your goal is to estimate Part B cost-sharing, always ask: “Is that based on the Medicare-approved amount?”

Open loop: why the same CPT can produce two different “you pay” totals

Keep this in your back pocket: cataract surgery cost-sharing can change when the setting changes, even if the procedure code looks the same. That’s why “ASC vs hospital outpatient” isn’t a trivia question. It’s often the lever that moves the facility side of your coinsurance.

ASC vs hospital outpatient: the setting choice that quietly changes your bill

In real life, “outpatient” gets used like it means “cheaper.” It doesn’t. There are two common outpatient settings for cataract surgery: an Ambulatory Surgical Center (ASC) and a Hospital Outpatient Department (HOPD). Your surgeon can be the same person in both places—yet your facility-side cost-sharing can shift.

Facility fee vs surgeon fee: which one moves when the setting changes

A simple mental model: the surgeon fee is tied to the professional service, and the facility fee is tied to the building. When you move from ASC to HOPD, you often move the facility side more than the surgeon side. I once watched a friend compare “surgeon quotes” only—then act shocked when the facility bill arrived later like an unwanted sequel.

Pattern interrupt: let’s be honest… “outpatient” is not a price guarantee

“Outpatient” describes where you sleep (usually at home), not what you pay. It’s like saying “I’m buying a sandwich” and expecting the price to be identical at a corner deli and an airport. Same noun. Different universe.

Decision card: when ASC vs hospital outpatient tends to matter most

- Your surgeon offers the same lens plan at an ASC

- You’re cost-sensitive and want to minimize facility-side variability

- Your billing office can provide a written ASC facility estimate

- You have medical complexity that the surgeon recommends in a hospital setting

- There’s a specific anesthesia or monitoring need

- The ASC option isn’t available in your area

Neutral next step: Ask both the surgeon and facility to confirm the setting in writing before you compare costs.

Open loop: the scheduling-sheet word that flips your estimate

The word is the facility type: “ASC” vs “hospital outpatient department.” It can be buried in a scheduling note, a portal message, or a rushed phone call. If you only do one “operator move” today, do this: ask, “Is my surgery scheduled at an ASC or a hospital outpatient department?”

Two bills, one procedure: how Medicare cataract surgery is commonly charged

Here’s the part that makes grown adults feel like they’re losing their minds: cataract surgery commonly creates two separate coinsurance obligations under Part B— one tied to the facility and one tied to the doctor. Medicare.gov spells it out plainly for hospital outpatient and ASC settings: after you meet the Part B deductible, you pay 20% of the Medicare-approved amount to both the facility and the doctor. If you want a deeper “why did I get multiple envelopes?” explanation, it helps to read a focused breakdown of a typical cataract surgery bill and how the charges split.

Bill #1: facility (ASC or HOPD) and what it tends to include

Think of the facility bill as “the room and the system”: supplies, nursing services, equipment, and the operating environment. Even if you never see an itemized list that feels satisfying, this is where “setting” often shows up financially. I once asked a facility for an estimate and got a number so neat it looked fictional—until I realized it only reflected the facility line, not the surgeon. (Neat numbers are suspicious. Life is not neat.)

Bill #2: surgeon/doctor (and sometimes anesthesia) — what to ask upfront

The professional bill is for the surgeon’s work. In some cases, you may also see separate charges related to anesthesia or other professionals, depending on how services are provided and billed. The point isn’t to memorize who bills what; the point is to refuse the “one-number fog.” Ask for the estimate in two buckets: facility and professional. If you want the coverage fundamentals in one place before you start calling, it helps to review how cataract surgery is typically covered under Medicare Part B.

Infographic: the “Two-Bill Map” (why one procedure becomes multiple payments)

- Setting-dependent

- Often the “quiet” driver

- Ask for written estimate

- More stable across settings

- Still must be confirmed

- Ask about assignment

Short Story: The quote that “forgot” the second bill (120–180 words) …

A family friend—retired, organized, the kind of person who labels cables—called me after getting a cataract surgery quote that felt oddly comforting. “They said my portion would be about a few hundred,” she said, as if she’d found a secret door in the maze. The quote came from the facility. It was real, but incomplete. Two weeks after surgery, her mailbox delivered the sequel: a separate professional bill.

She didn’t do anything wrong. She just didn’t know the system prefers multiple envelopes. We sat at the kitchen table, made tea, and rebuilt the estimate the way it should have been built from the start: facility line, professional line, deductible status, assignment question, and a separate category for upgrades. Nothing magical. Just clear buckets. Her stress dropped the moment the fog turned into columns.

- Ask for two buckets: facility + surgeon

- Expect bills to arrive at different times

- Separate upgrades into their own category

Apply in 60 seconds: Text yourself: “Two bills. Two estimates. Two confirmations.”

Open loop: why bills arrive weeks apart (and why that matters for budgeting)

Different entities bill on different timelines. It can feel personal, like the system is testing your patience. It’s not. It’s administrative reality. Budgeting-wise, it matters because you may pay the facility coinsurance first, then the professional coinsurance later. If cash flow is tight, plan for a staggered landing rather than one clean splash.

Show me the nerdy details

Medicare Part B cost-sharing is typically applied per covered service or item after the annual deductible is met. When services are billed by different entities (facility vs physician), you can see separate explanations of benefits and separate patient responsibility amounts. That’s why “the procedure” can feel like it fractured into pieces—even when clinically it was one event.

Medicare.gov lookup workflow: turn CPT 66982 into a usable estimate

Medicare’s Procedure Price Lookup is the closest thing to an official “compare settings” lens that normal humans can use without a billing degree. It’s designed to show national-average estimates and help you compare how costs may differ between an ASC and a hospital outpatient department. For CPT 66982 (often used for complex cataract surgery), the tool displays a “patient pays (average)” figure and lets you toggle the setting.

What the tool is designed to do (and what it isn’t)

Use it for directional comparison—ASC vs hospital outpatient—especially when you don’t yet have written estimates. Don’t use it as your final invoice. It won’t know your exact clinical details, your local contracted patterns, or whether you’re choosing elective upgrades.

National average vs ZIP reality: how to avoid false precision

Treat the lookup as a weather forecast: useful, not perfect. Your ZIP and local pricing can change the numbers. If you’re the kind of person who wants a single “exact” dollar amount, I say this gently: Medicare billing is not a single number until you’ve confirmed the facility and professional sides in writing.

Here’s what no one tells you: the lookup may not reflect every bill you’ll receive

The lookup is excellent for what it is—comparison. But your real-life experience can still involve separate bills. That’s not a flaw in the tool; it’s a feature of how billing is organized. Use the lookup to get your bearings, then use calls and written estimates to lock it down.

Quote-prep list: what to gather before you compare prices

- The setting: ASC or hospital outpatient department

- The procedure code if provided (commonly discussed: 66982 for complex; your case may differ)

- Whether the surgeon and facility accept assignment

- Whether you’re considering premium lens or other elective add-ons

- Your deductible status for the calendar year

Neutral next step: Use this list as your call script header before you ask for numbers.

Inputs that matter: the 7-field worksheet for your personal estimate

Most billing confusion comes from missing inputs, not from complicated math. When you give a billing office clear inputs, you’re more likely to get a clean estimate. When you give vague inputs, you get the dreaded “range” that covers basically every possible reality. (I once heard an estimate range so wide it could have been describing a used car market.)

Field 1: deductible status (met vs not met)

Deductible status changes the first dollars you pay. If you’ve already had other Part B services in 2026, your deductible may be partially or fully met. If not, assume it applies. Either way, ask the billing office to note your assumption.

Field 2: setting (ASC vs hospital outpatient)

Confirm the setting in writing. Don’t rely on “outpatient” alone. If the office says, “It’s at the hospital,” ask whether it’s an ASC located near a hospital campus or a hospital outpatient department. Yes, it feels awkward. Yes, it saves money questions later.

Field 3: assignment acceptance (yes/no)

Medicare’s own language is simple: if a provider accepts the Medicare-approved amount as full payment, that’s called accepting assignment. It matters because it affects how “surprises” show up. Ask both the surgeon and the facility: “Do you accept assignment for this procedure in this setting?” If you want the practical “what to check before you commit” version, the Medicare Part B cataract surgery coverage guide is a helpful reference point.

Field 4: one eye vs second eye timing (calendar-year reset risk)

If you do one eye late in the year and the second eye early the next year, you might cross a calendar-year deductible boundary. I’ve seen people plan surgery dates around family visits, then later realize the deductible resets on January 1. No guilt—just awareness.

Field 5: lens type (standard vs premium)

Medicare Part B may cover cataract surgery that implants conventional intraocular lenses, and Medicare.gov notes it also covers one pair of eyeglasses with standard frames (or one set of contacts) after each cataract surgery that implants an intraocular lens. If you want the “what counts, what doesn’t, and when it resets” version, see the Medicare cataract surgery glasses rule and the companion breakdown of glasses coverage after cataract surgery. Premium lenses and packaged upgrades are where quotes can inflate. Which leads us to…

Field 6: astigmatism correction / laser add-ons (elective vs medically necessary)

Some add-ons are presented like “the modern way,” which is a marketing sentence, not a coverage sentence. The operator move is to ask for itemization: covered portion vs elective portion.

Field 7: pre/post care & drops (bundled vs billed separately)

Some practices bundle post-op care and routine follow-ups; others bill separately. Eye drops can also be a separate cost category (often influenced by your drug coverage). Ask: “Are post-op visits included? Are drops included? If not, what should I plan for?” If dry, scratchy eyes show up during recovery, it may help to keep a separate note on preservative-free tears after cataract surgery so “comfort care” doesn’t get mixed into your surgery-cost math.

Show me the nerdy details

Your estimate becomes more accurate when each input is tied to a specific bill category: facility-approved amount, professional-approved amount, and a separate list for non-covered upgrades. When offices can’t or won’t itemize, you can still reduce uncertainty by locking the setting, confirming assignment, and separating “covered surgery” from “optional upgrades.”

Upgrade trap control: premium lenses & laser packages without sticker shock

Upgrades are where people get emotionally whiplashed. The conversation starts as, “Medicare covers cataract surgery,” then slides into, “Would you like the premium lifestyle lens package?” Nothing is wrong with wanting better vision goals. The problem is when the quote blends covered and non-covered items into one foggy number.

Standard lens vs premium IOL: how quotes inflate without warning

If your practice offers monofocal, toric, multifocal, or other specialty options, you may see price differences. The coverage reality can vary depending on what is medically necessary versus elective. Your job is not to debate lens physics. Your job is to force a clean financial separation: “Please itemize what Medicare covers and what I would pay out-of-pocket as an elective upgrade.” If you want a “what are these options actually called?” reference to keep the conversation grounded, see monofocal vs multifocal vs toric IOL.

Astigmatism correction: when it becomes an elective add-on

Sometimes astigmatism-related correction is framed as a must-have. Sometimes it’s truly helpful. Sometimes it’s optional. The safe path is the same: itemize, and make a decision with numbers, not vibes. (I say this as someone who once bought “optional” concert-hall seats and later realized “optional” meant “expensive.”)

Quick reality check: “bundled upgrades” often hide non-covered line items

Bundles can be convenient. Bundles can also be camouflage. Ask for a printed breakdown with line items—covered vs not covered—before you commit. If you want a dedicated checklist for this exact moment, use premium lens upgrades: how to avoid sticker shock and “bundle fog”.

- Ask for itemized upgrades in writing

- Confirm setting and assignment first

- Don’t compare an upgraded quote to a “standard” quote without matching categories

Apply in 60 seconds: Ask: “Can you print the covered portion separately from the elective portion?”

Coverage tier map: what changes from “standard” to “premium quote”

- Part B deductible (if not met)

- 20% coinsurance on approved amounts

- Conventional lens pathway

- Premium lens components (if elective)

- Elective laser-related packages (if offered)

- Extra diagnostics not included in baseline estimate

- Single price with no line items

- Covered and elective blended together

- No clarity on facility vs surgeon amounts

Neutral next step: Request the Tier 1 number first, then decide on Tier 2 intentionally.

Common mistakes: the 5 ways people accidentally pay more

This section is a little tough-love, because it saves real money and real stress. I’ve made versions of these mistakes myself—mostly out of optimism and a desire to be “easy.” Medicare billing is not a place where being “easy” pays you back.

Mistake #1: treating the deductible like a one-time lifetime fee

The Part B deductible is annual. It resets each calendar year. If you’re scheduling around travel or family events, check whether your surgery plan crosses January 1.

Mistake #2: comparing only the facility estimate and skipping the surgeon line

This is the classic “quote that forgot the sequel.” Always confirm both buckets. If an office can only provide one bucket, ask them to tell you who provides the other—and how to reach them.

Mistake #3: assuming “Medicare covers 80%” means your 20% is always small

20% of a small approved amount is small. 20% of a larger total is not small. The percentage is stable; the approved amount is the moving piece.

Mistake #4: not asking “Do you accept assignment?” (and why it’s a money question)

Assignment isn’t a personality trait. It’s a billing practice. When providers accept the Medicare-approved amount as full payment, your estimate has fewer hidden doors. Ask the question calmly, like you ask whether a restaurant takes reservations.

Mistake #5: letting “upgrade talk” start before you see an itemized quote

Upgrades are easiest to choose when you know your baseline. Otherwise, you’re comparing a luxury package to an unknown default. Get the Tier 1 number first. Then shop with clarity.

Who this is for / not for: right reader, right calculator

This calculator approach is designed for one specific situation: Original Medicare (Part B) and a desire to estimate cost-sharing using the deductible-and-coinsurance structure. If that’s you, you’re in the right place. If not, you may need a different framework.

For: Original Medicare Part B planning + comparing settings

You’ll get the most value if you: (1) want a do-the-math estimate, (2) can choose between ASC and hospital outpatient, and (3) are willing to request written estimates from both the surgeon and the facility.

Eligibility checklist (yes/no)

- Yes — You’re enrolled in Original Medicare and using Part B for outpatient services

- Yes — You want to compare ASC vs hospital outpatient costs

- Yes — You can request written estimates from both the facility and surgeon

- No / Not sure — You’re in Medicare Advantage (Part C) with plan-specific rules

- No / Not sure — You’re using VA benefits or a cash-bundle package with separate pricing logic

Neutral next step: If any “Not sure,” call your coverage administrator (plan or benefits office) before relying on this estimate method.

Not for: Medicare Advantage (Part C), VA, or cash-bundle pricing (different rules)

Medicare Advantage often uses plan-specific networks, prior authorization rules, and cost-sharing designs that don’t map cleanly to “Part B deductible + 20%.” Cash bundles can be transparent and convenient—but they are their own ecosystem. In those cases, you’ll want a plan-specific or contract-specific estimate approach.

When to seek help: symptoms after cataract surgery that aren’t “wait-and-see”

A quick safety section—because money planning shouldn’t crowd out health signals. Many people have mild discomfort after cataract surgery, but certain symptoms deserve urgent attention. If anything feels “wrong-wrong,” trust that instinct and contact your surgeon’s office right away.

Urgent: sudden vision drop, severe/worsening pain, increasing redness, flashes/floaters, nausea/vomiting

These can be red flags. If you experience severe pain, a sudden decrease in vision, rapidly increasing redness, new flashes or a shower of floaters, or intense nausea/vomiting, treat it as urgent. Call your surgeon’s emergency number or seek immediate care if you can’t reach them. For a fuller, plain-English safety overview, see cataract surgery complications in seniors.

If you can’t reach the surgeon: where to go and what to say

If you can’t get through, go to an urgent/emergency setting and say plainly: “I recently had cataract surgery and I have new/worsening symptoms.” Keep it simple. Clarity beats bravery.

FAQ

What is the Medicare Part B deductible in 2026?

CMS announced the annual Part B deductible is $283 for 2026. It’s paid once per calendar year before Original Medicare begins paying for most Part B-covered services.

Do I always pay 20% coinsurance for cataract surgery with Medicare?

For covered cataract surgery under Part B, the common structure is: after you meet the Part B deductible, you pay 20% of the Medicare-approved amount. Your exact totals can vary based on setting, billing practices, and whether there are non-covered upgrades.

Do I pay coinsurance to both the facility and the surgeon?

For cataract surgery performed in a hospital outpatient setting or ambulatory surgical center, Medicare.gov explains that after the Part B deductible, you typically pay 20% of the Medicare-approved amount to both the facility and the doctor. That’s why “two bills” is a helpful default assumption.

Is cataract surgery cheaper in an ASC than a hospital outpatient department?

Often it can be, but it’s not guaranteed. The most reliable way to compare is to use Medicare’s Procedure Price Lookup to compare settings, then confirm the setting and request written estimates from both the facility and the surgeon.

What does “Medicare-approved amount” mean for my bill?

It’s the amount Medicare recognizes for a service in a specific setting. Your coinsurance is typically a percentage of this approved amount, which can differ from a provider’s “standard charge” or cash price.

What does it mean if my doctor “accepts assignment”?

Medicare uses “assignment” to describe a provider accepting the Medicare-approved amount as full payment. It’s a key question because it affects how predictable your estimate is and helps reduce surprise billing dynamics.

Does Medicare cover premium lenses (toric/multifocal) or laser cataract surgery?

Medicare Part B may cover cataract surgery with conventional intraocular lenses, but elective upgrades can create additional out-of-pocket costs. The safest approach is to request itemized quotes that separate covered services from elective upgrades before you decide.

If I do the second eye later, do I pay the deductible again?

The Part B deductible is annual. If your surgeries fall in different calendar years, you may face a new deductible in the new year. If both surgeries occur in the same year, you generally don’t “re-pay” the deductible once it has been met.

Can I get a written estimate before scheduling—and what should it include?

Yes, you can request a written estimate. Ask for two buckets (facility and professional), confirmation of setting (ASC vs hospital outpatient), whether they accept assignment, and an itemized list of elective upgrades with separate pricing.

Next step: the 10-minute “no-surprise” call script (surgeon + facility)

This is the part where you stop guessing. Two calls, one goal: a number you can trust—or a clear reason you can’t yet. I’ve used versions of this script enough times that I can feel my shoulders drop as soon as the office answers with specifics. Specifics are calming. Vague bundles are not.

- Confirm ASC vs hospital outpatient in writing

- Ask if they accept assignment

- Separate covered care from elective upgrades

Apply in 60 seconds: Copy/paste the script below into your notes app before you call.

Call script (copy/paste)

Start with the setting:

- “Can you confirm whether my cataract surgery is scheduled at an ASC or a hospital outpatient department?”

- “Can you put that setting in the written estimate or portal message?”

Then the billing practice:

- “Do you accept assignment for this procedure in this setting?”

- “Is your estimate based on the Medicare-approved amount?”

Then the two buckets:

- “Please provide the estimate in two parts: facility and professional/surgeon.”

- “If you don’t provide the other part, who does? What number should I call?”

Finally, the upgrade separation:

- “If there are premium lenses or other add-ons, can you itemize them separately from the covered portion?”

- “Can you print the covered portion alone so I can compare ASC vs hospital outpatient fairly?”

Neutral next step: If the office can’t itemize, ask for a written baseline estimate first and discuss upgrades only after you have it.

Show me the nerdy details

This script is designed to reduce “estimate variance.” It forces four clarifying constraints: (1) lock the setting, (2) confirm assignment, (3) split facility vs professional, and (4) separate elective upgrades. If you do these in this order, you dramatically reduce the chance that you compare mismatched numbers.

Conclusion: lock your estimate in 15 minutes

Remember the curiosity loop from the start—the mystery math? Here’s the honest ending: the math was never the hard part. The hard part was that the system likes to speak in bundles while your budget needs columns.

Your fastest path to clarity is this: use the deductible-and-coinsurance baseline, compare ASC vs hospital outpatient with Medicare’s lookup tool, and then do the two calls with a script that forces the “two-bill reality” into daylight. It’s not glamorous, but it works. And it gives you back that quiet feeling of control—like stepping into a concert hall just before the music starts, when the noise fades and you can finally hear what matters.

Your 15-minute next step: Open your notes app, copy the call script, run the Procedure Price Lookup, and make the surgeon + facility calls back-to-back.

Last reviewed: 2026-01