How to Read Your Cataract Surgery Bill: 7 Shocking Errors I Made

My Biggest Mistake After Cataract Surgery? Thinking the Bill Would Be Just One.

I genuinely believed I’d get a bill. Singular. A nice, clean summary of what I owed for the whole thing. Cataract surgery: check. One invoice: check. Pay it, done.

Yeah… no.

Instead, what landed in my mailbox (and inbox, and portal inbox, and one time in a random voicemail) was a parade of mystery charges from people I swear I never met. One from the surgeon. One from the facility. Another from some anesthesiologist whose name I had to Google to confirm was a real person. Then came a “surgical assistant” charge—someone I’m 98% sure didn’t introduce themselves or even make eye contact.

If you’re in the middle of recovery, working, managing life, and just trying to figure out what the heck you actually owe, this guide is for you.

I’ll break down the exact patterns that trip up smart, busy people like us—stuff that makes even organized folks say, “Wait, did I pay this already?” or “Was this not covered?”

We’ll go over:

- The 7 common mistakes most people make with medical billing (yes, I made all 7, thanks for asking),

- How to spot and decode confusing line items,

- And the quick checks that can save you 20–30 minutes per statement—and sometimes real money.

We’re keeping this practical, a little ruthless, and completely doable—even if you’re foggy from eye drops and just want to lie down.

Table of Contents

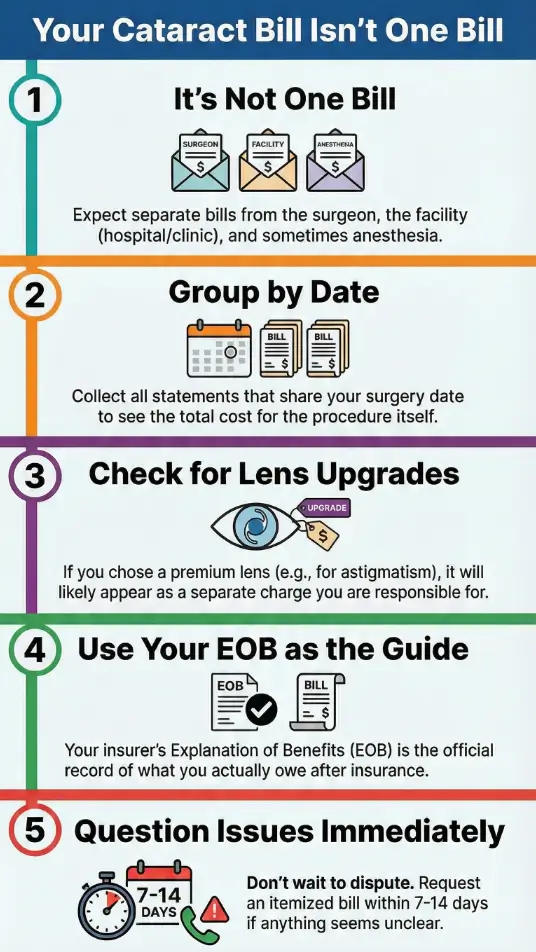

What a cataract surgery bill usually includes

The first thing that tripped me up was the architecture. Cataract surgery billing often arrives as a set of related claims, not a single neat invoice. Even when the clinical day feels like one smooth appointment, the financial side can split into multiple paths.

In plain English, you may see:

- Surgeon’s professional fee

- Facility fee (hospital outpatient department or ambulatory surgery center)

- Anesthesia-related charges (sometimes minimal, sometimes separate)

- Lens-related line items if you selected an upgrade

- Post-op visits and prescriptions

A small but important reality check: these items can arrive across 2–6 separate statements over a few weeks. That spread alone creates confusion, especially when you’re juggling work, rides, and eye drops that demand the punctuality of a train schedule.

- Expect multiple statements

- Match dates of service across documents

- Lens upgrades can create extra lines

Apply in 60 seconds: Write the surgery date at the top of each bill and group everything by that date.

The 7 errors at a glance

Here’s the fast map of what tends to go wrong. I’m framing these as “errors I made” because that’s the emotional truth of the experience: the bill doesn’t just demand math, it demands calm.

- Error #1: I treated the pre-op estimate like the final truth.

- Error #2: I didn’t confirm the exact provider identity and location.

- Error #3: I forgot the surgeon, facility, and anesthesia can bill separately.

- Error #4: I skimmed past the lens upgrade line item.

- Error #5: I ignored codes and modifiers that changed the patient share.

- Error #6: I underestimated post-op meds and follow-ups.

- Error #7: I waited too long to challenge an item.

Think of this guide as your bill translator. We’re not hunting perfection. We’re hunting clarity.

Error #1: Confusing the estimate with the final claims

The estimate felt reassuring. It was a friendly spreadsheet with polite numbers. The final claims felt like a different universe.

Estimates are often built on expected coverage and typical coding patterns. Real life adds small variables: a different facility classification, a lens choice you barely remember agreeing to, or an insurer rule that turns on one detail of your plan year.

What I should have done in the first 5 minutes after receiving the estimate:

- Ask whether the estimate separates professional vs facility charges.

- Confirm whether it assumes a standard monofocal lens.

- Request a written note of the billing office contact.

That tiny discipline reduces the “why is this number different?” spiral later.

Error #2: Not matching the provider identity and location

One line on my statement used a name I didn’t recognize. I panicked for 12 seconds, then did what most people do: I ignored it and hoped it would make sense later. It didn’t.

Hospitals and surgical centers can bill under parent entities, physician groups, or facility brands that sound like distant cousins of the clinic you actually visited.

Two quick checks that usually clarify this:

- Date of service match: Does the charge align with your surgery date or a post-op visit?

- Location match: Is it tied to the hospital outpatient department or an ambulatory surgery center?

This matters because facility type can change how your plan applies deductibles or coinsurance.

- Match date of service first

- Confirm facility vs clinic

- Keep screenshots of appointment confirmations

Apply in 60 seconds: Call the billing number and ask, “Which entity name should I expect on my statements for this surgery?”

Error #3: Forgetting that surgeon, facility, and anesthesia bill separately, 2025 (US)

This was the most “how did I not know this?” moment. The surgery day felt like one purchase. The billing system treated it like a small orchestra where each instrument invoices you in its own tempo.

In the United States, it’s common to receive at least two major claims streams:

- Professional services (the surgeon)

- Facility services (the site where the surgery happened)

Anesthesia-related billing can also appear separately depending on the setting and documentation.

Decision card:

- Scenario A: One large facility charge + smaller surgeon charge.

- Scenario B: Smaller facility charge but a noticeable lens upgrade or added services.

- Your next step: Ask for an itemized statement from each entity.

Apply in 60 seconds: Create three folders in your notes app: Surgeon, Facility, Anesthesia. Drop PDFs as they arrive.

This one simple habit can save you 20–30 minutes of backtracking later.

- Yes/No: Is your cataract surgery being billed as medically necessary rather than elective?

- Yes/No: Do you have active coverage on the surgery date and the facility is in-network?

- Yes/No: Did you choose a premium lens that may trigger non-covered upgrade charges?

Next step: If any answer is “No” or “Not sure,” request the planned billing codes and facility name in writing before you pay. Save this checklist and confirm the current plan rules on your insurer’s official page.

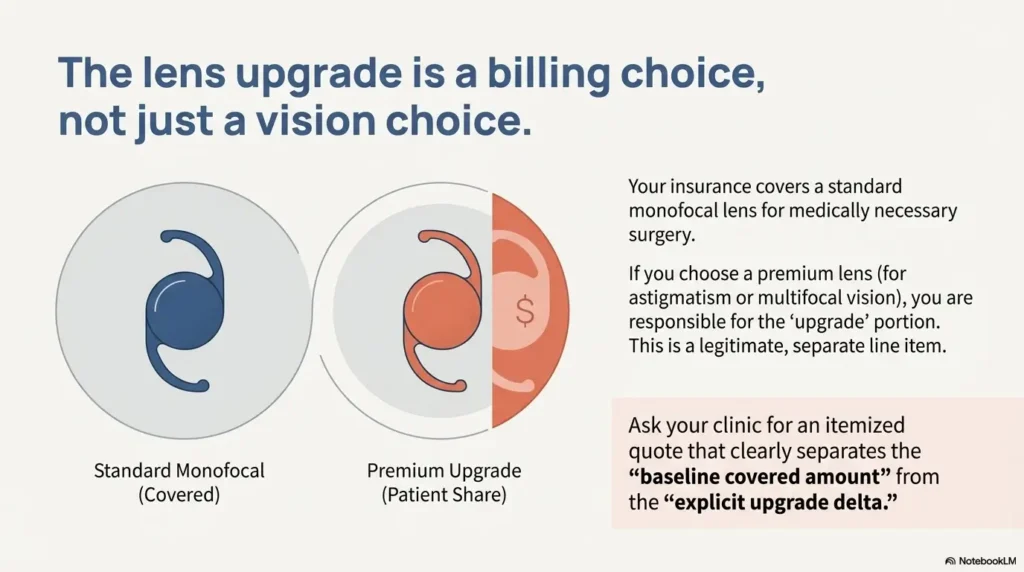

Error #4: Missing the lens upgrade line item

If there’s one place where patients get blindsided, it’s the lens conversation that felt simple in the exam room and becomes complicated on paper.

Many plans cover a standard monofocal lens as part of medically necessary cataract surgery. But if you select a premium option—like toric for astigmatism or an extended depth-of-focus lens—you may see a separate “upgrade” charge.

I used to think the lens decision was a “vision preference” choice. It’s also a billing choice.

Coverage tier map (conceptual, not a promise):

- Tier 1: Standard monofocal lens (commonly treated as the baseline covered option)

- Tier 2: Astigmatism-correcting options

- Tier 3: Multifocal or EDOF options

- Tier 4: Combined upgrades with additional refractive goals

- Tier 5: Custom packages bundled by clinics

The exact financial impact hinges on your insurer and the clinic’s upgrade policy. The point is not to fear upgrades—it’s to see them clearly on the bill and verify that the baseline portion was still applied correctly.

- Ask for a written upgrade quote

- Confirm the baseline lens credit

- Keep the lens consent form

Apply in 60 seconds: Request an itemized lens upgrade sheet that separates covered vs non-covered components.

Error #5: Not checking the codes and modifiers

I know. This is the part where eyes glaze over—ironically, after an eye procedure.

But a quick glance at codes can tell you whether the claim is aligned with what you actually had done. For cataract surgery in the U.S., you may see common procedure codes such as 66984 (routine cataract extraction with IOL insertion) or 66982 (complex cataract surgery). The difference can affect reimbursement pathways and sometimes the patient share depending on plan rules.

What I look for now:

- Does the code align with “routine” vs “complex” notes you heard pre-op?

- Do right/left eye indicators match your surgery?

- Is the date of service correct?

Show me the nerdy details

Billing systems map procedure codes to payer-specific fee schedules and coverage logic. A single modifier or laterality mismatch can cause a claim to route incorrectly, triggering a denial or shifting a portion to patient responsibility. You don’t need to master coding—just verify that the code category and eye-side match your actual care.

That 2-minute check can prevent a longer appeal later.

- Surgery date and facility name

- Surgeon group billing contact

- Lens choice paperwork and any upgrade quote

- Your plan’s deductible and coinsurance status for the year

- All EOBs related to the surgery

Apply in 60 seconds: Put these into a single phone note titled “Cataract Bill Packet.” Save this list and confirm today’s rules on your insurer’s official page.

Error #6: Overlooking post-op medications and follow-ups

I mentally budgeted for the procedure and forgot the “quiet costs” that come after. The eye drops, the pharmacy copays, and the follow-up visits can be small individually but annoying in aggregate.

Two practical truths:

- Post-op visits may be bundled in some billing models, but that’s not universal.

- Medication costs can vary by formulary tier and pharmacy network.

If your plan uses tiered pharmacy pricing, a brand-name steroid or antibiotic drop can feel disproportionate. This is where asking for a therapeutic alternative can sometimes help—without compromising care.

Micro habit that saved me stress: I set a reminder for Day 3 after surgery to check whether the pharmacy receipt matched what the clinic said to expect. Catching surprises early is calmer than untangling them when the entire drop schedule has already blurred together.

Error #7: Waiting too long to dispute or appeal

This one is painfully human. You’re healing. Your vision is adjusting. You’re tired. The bill arrives, and your brain politely files it under “future me will deal with this.”

But billing systems often have time windows for corrections or appeals. The exact timeframe depends on the payer, provider, and jurisdiction. The practical rule is simple:

- Start your questions within 7–14 days of receiving the first confusing statement.

- Ask for an itemized bill before you pay a disputed amount.

- Document the name and date of every call.

You don’t need to be adversarial. You just need to be early.

Short Story: The “three envelopes” week

Three envelopes arrived in five days. The first looked like a polite summary. The second had a different logo and a number that felt like it belonged to someone else. The third was an explanation-of-benefits that read like a riddle written by a bored accountant. I remember thinking, “I can read dense policy documents for work—why is this making me sweat?” What calmed me wasn’t a magic phone call.

It was a tiny system: one note on my phone labeled with the surgery date, three subfolders for surgeon, facility, and pharmacy, and a rule that I would never react emotionally until I matched the date and the entity. The confusion didn’t disappear overnight. But within a week, the bills stopped feeling like random lightning and started feeling like a map I could actually walk.

60-second out-of-pocket estimator

This is a back-of-the-envelope tool to help you sanity-check your expectations. It won’t replace your insurer’s official numbers, but it can help you spot when something feels wildly off.

Enter only what you know. If you don’t know an item, leave the default.

Estimated patient share: $0

This assumes your plan applies deductible first, then coinsurance. Real rules may differ by plan and facility type.

Apply in 60 seconds: If your bill is far above this rough estimate, request an itemized bill and verify network status and lens upgrade details on the provider’s official page.

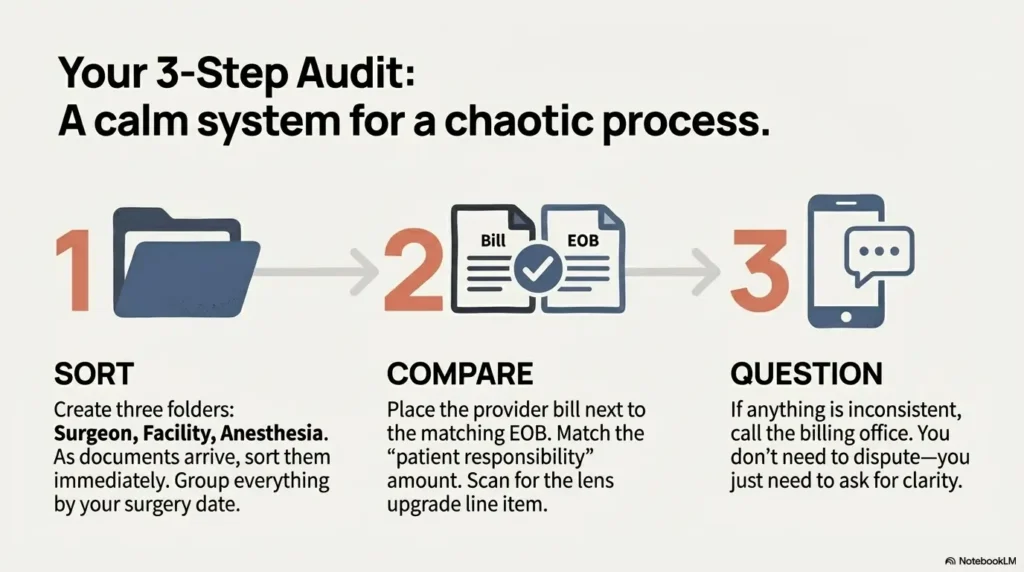

A simple bill-audit workflow you can use today

If you only remember one process from this article, make it this. It’s built for real life and limited energy.

- Group by entity: surgeon, facility, anesthesia, pharmacy.

- Match dates: surgery day vs follow-ups.

- Cross-check with your EOB: the insurer’s version of the story.

- Scan for upgrades: lenses, refractive add-ons, special packages.

- Request itemization early if anything feels inconsistent.

Humor moment I allow myself now: If a bill arrives with a logo I’ve never seen, I no longer assume doom. I assume paperwork. That shift alone saves a few mental calories.

| Bucket | What it covers | Why it surprises people |

|---|---|---|

| Surgeon | Professional services for the procedure | Often arrives separately from facility paperwork |

| Facility | Operating room, staff, supplies, site-based costs | Setting type can change plan cost-sharing |

| Anesthesia | Monitoring and sedation-related services where applicable | May be billed by a separate group |

| Lens upgrade | Patient-elected premium lens or refractive package | Baselines vs upgrade credits get blurred |

| Post-op meds | Drops and related pharmacy items | Formulary tiers can shift copays unexpectedly |

Apply in 60 seconds: Save this table and confirm the current fee logic on the provider’s official page.

A quick US localization note

Because billing rules vary dramatically by country, this article assumes you’re navigating the U.S. ecosystem of private insurance, Medicare, and facility-based claims. If you’re outside the U.S., the structure of the troubleshooting still helps—group by entity, match dates, request itemization—but the exact coverage logic and patient share calculations will follow your national system’s rules.

What to say on the phone so you don’t lose 30 minutes

When you call billing, you want clarity, not a duel. These phrases keep the conversation efficient:

- “Can you send an itemized bill for this date of service?”

- “Which part is surgeon vs facility?”

- “Is there a separate lens upgrade charge, and what baseline credit was applied?”

- “Can you confirm the network status for the facility and any anesthesia group?”

That script can cut the call from 25 minutes to something closer to 10–12, especially if you already have your EOB nearby.

When a bill error is actually an EOB mismatch

Sometimes the provider bill looks wrong because you’re missing the insurer’s companion document. The EOB is where you see:

- What was billed

- What your insurer allowed

- What the insurer paid

- What you may owe

If the provider statement requests payment that doesn’t match the EOB, that’s your cue to pause and ask for clarification before paying.

- Don’t pay a disputed amount first

- Match allowed vs billed

- Request corrected statements in writing

Apply in 60 seconds: Put the EOB and provider bill side-by-side and highlight any mismatch line.

External research and official guidance

If you want to verify coverage language or patient rights from authoritative sources, these pages are a solid starting point.

Infographic: 2025 cataract bill roadmap

Gather all statements for 2–6 weeks after surgery.

Surgeon • Facility • Anesthesia • Pharmacy.

Surgery day vs follow-up visits.

Look for baseline vs premium upgrade separation.

Allowed vs billed vs patient share.

Request itemization within 7–14 days if unclear.

What to do if you chose a premium lens and regret the paperwork

This is more common than anyone admits. The choice can be clinically reasonable and financially surprising at the same time.

Two calm steps:

- Ask for the baseline-covered amount and the explicit upgrade delta.

- Request a copy of the signed lens election or consent form.

This isn’t about conflict. It’s about reconstructing the story of the transaction so your bill matches your memory.

The quiet role of deductibles and plan-year timing

Another subtle trap: the same surgery can feel cheaper or pricier depending on where you are in your plan year.

If your deductible resets in January, a surgery in late December can play out differently than one in early January. This is boring, but it matters.

Two numbers worth checking:

- Your remaining deductible before the surgery date

- Your coinsurance percentage for outpatient procedures

Even a quick confirmation of those two items can reshape your expectations and reduce the shock later.

Two more authoritative pages to verify details

For clinical background and broader patient guidance, these organizations are widely trusted.

FAQ

Why did I get separate bills for one cataract surgery?

Because the surgeon, facility, anesthesia group, and pharmacy may bill independently. The fastest fix is to group statements by entity and match the surgery date across them. Apply in 60 seconds: Create four folders in your phone or email and sort every new document immediately.

What if the provider name on the bill doesn’t match my clinic?

This is often a parent organization or billing entity. Confirm the date of service and location first, then ask billing to explain the exact relationship. Apply in 60 seconds: Call and ask, “What legal entity name should I expect for this procedure?”

How do I know if a lens upgrade charge is legitimate?

Ask for a line-by-line breakdown that separates the baseline covered lens amount from the elective upgrade portion. Compare it with your signed lens election form. Apply in 60 seconds: Request the upgrade quote and consent form by email.

Do I have to pay before I request an itemized bill?

You can usually request itemization before paying a disputed amount. It’s reasonable to pause payment while you verify that your EOB and provider statement align. Apply in 60 seconds: Send a short message: “Please provide an itemized statement for this date of service.”

What should I do if my bill doesn’t match my EOB?

Treat it as a reconciliation issue. Ask the provider to re-check claim status and confirm whether any adjustments are pending. Apply in 60 seconds: Highlight the mismatch line and read it verbatim to billing.

Conclusion: What I wish I had done in the first 15 minutes

The curiosity loop from the start deserves a clean answer: the bill felt chaotic because I expected a single tidy receipt for a multi-entity process.

If I could rewind the clock, I’d spend 15 minutes doing three things:

- Open a note titled with the surgery date.

- Sort every document into Surgeon, Facility, Anesthesia, Pharmacy.

- Compare the first EOB to the first provider statement before paying anything unclear.

That’s it. No heroics. No medical-degree cosplay. Just a calm system that respects your time.

Your next step today: Run the mini estimator above, then request itemized bills from any entity that doesn’t clearly match your EOB. If you chose a premium lens, ask for the baseline credit breakdown in writing. You’ll move from “what is this?” to “I understand exactly what I’m paying for” faster than you think.

Last reviewed: 2025-12. cataract surgery bill, cataract surgery cost, EOB explanation, premium IOL, medical billing disputes