Navigating the “One Pair” Rule: Avoiding the Post-Cataract Upgrade Trap

“Covered” is how a lot of people end up paying full price at the optical counter—because the bill is born in one quiet line item: upgrade.

Here’s the clean truth: Medicare’s “one pair of glasses” rule after cataract surgery is real, but it’s narrow, procedural, and easy to miss if the shop defaults you into a retail workflow. (If you want the big picture first, start with this Medicare cataract surgery glasses coverage overview and come back for the checkout-proof details.)

Definition (The part people mishear):

After cataract surgery with an implanted intraocular lens (IOL), Medicare Part B generally covers one pair of eyeglasses with standard frames (or one set of contact lenses) per surgery—subject to deductible/coinsurance and limited to what Medicare allows. Extras (premium frames, coatings, specialty lenses) usually land in “upgrade” territory.

Keep guessing, and you risk paying retail twice: once for timing, once for assumptions. This post helps you buy the right way—with a written covered vs. upgrade split, the right supplier, and a simple cost sanity-check before you swipe.

I learned this the hard way: the rule isn’t confusing—checkout is.

Slow down for 90 seconds. Use the process, not the vibe. Then shop frames with joy, not suspicion.

Table of Contents

- It’s typically glasses with standard frames OR contacts (you choose one)

- It applies after each cataract surgery that includes an implanted lens

- Your out-of-pocket depends on deductible, coinsurance, and upgrades

Apply in 60 seconds: Before you order, ask for an itemized “covered vs upgrade” breakdown in writing.

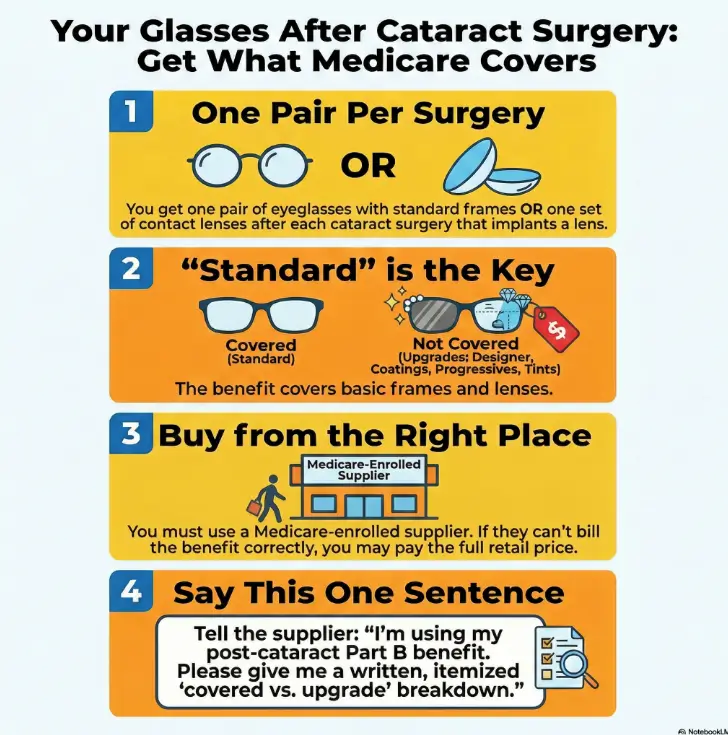

1) Rule decoded: what “one pair” actually refers to

Medicare Part B generally doesn’t cover routine eyeglasses—but after cataract surgery, it makes a specific exception: one pair of eyeglasses with standard frames (or one set of contact lenses) after each cataract surgery that implants an intraocular lens (IOL). That’s the sentence that gets quoted everywhere… and misunderstood everywhere.

“After each surgery” means per cataract surgery with an IOL

The trigger isn’t “my vision changed” or “my glasses are old.” The trigger is the surgery itself—specifically, cataract surgery where an IOL is implanted. If you have surgery on one eye now and the second eye later, think of it as two separate “events,” each with its own post-surgery eyewear benefit. (If you’re planning the timeline, this guide on cataract surgery one eye or both can help you think through staged vs. same-day decisions.)

Quick personal note: the first time I heard this, I assumed “one pair” meant “one for the whole cataract season of life.” The actual logic is closer to a receipt: surgery happens, then Medicare recognizes a limited corrective-lens benefit tied to that procedure.

Glasses or contacts: you pick one benefit type (not both)

You get to choose which benefit fits your life: eyeglasses (standard frames) or contact lenses. You don’t get both for the same surgery. If you’re a longtime contact lens wearer, this is the moment to pause and choose intentionally—not impulsively at checkout.

The hidden keyword: Medicare treats these as a prosthetic benefit after IOL surgery

This is the “why” behind the exception: an implanted lens (pseudophakia) changes how Medicare classifies the post-op correction. The coverage sits in a different bucket than routine vision benefits—so the paperwork, billing pathway, and supplier rules matter more than people expect. (If you’re still deciding lens type, bookmark monofocal vs multifocal vs toric IOL—it changes both vision expectations and the “upgrade” conversation later.)

Show me the nerdy details

In Medicare language, post-cataract corrective lenses are typically treated as a covered item after an IOL insertion, even though routine eyewear is excluded. That classification is why the claim flow often routes through suppliers and Medicare Administrative Contractors (MACs), and why “standard” coverage is tightly defined.

- What it means: A real benefit exists—but only in a narrow, post-surgical lane.

- What it doesn’t mean: Medicare suddenly becomes a general vision plan.

“One pair” is not a shopping allowance. It’s a post-surgery benefit with boundaries.

2) Who this is for / not for: the quick self-check

Think of this section like a fast fork in the road—because the biggest frustration I see is when people bring “routine eyewear expectations” into a “post-cataract benefit process.” Same products, different rules, different outcomes.

For you if: you had cataract surgery with IOL implantation and need corrective lenses

If you had cataract surgery and an IOL was implanted, and you need corrective lenses afterward, you’re in the right place. This benefit often applies whether you’re new to glasses or you’ve worn them for decades.

Not for you if: you’re shopping for routine eyewear, sunglasses, or “I just want a spare pair”

If your goal is “a backup pair,” “cute frames for weekends,” or prescription sunglasses, Medicare’s post-cataract rule usually won’t behave the way you want. You can still buy those things—just don’t count on Medicare to pay for them.

Caregiver note: what to ask the surgeon’s office before you buy

- Was an intraocular lens (IOL) implanted?

- When will the prescription be stable enough for new lenses?

- Do you have a recommended Medicare-enrolled supplier list—or a billing contact who can confirm requirements?

- Yes/No: Did you have cataract surgery with an implanted intraocular lens (IOL)?

- Yes/No: Are you choosing either glasses (standard frames) or contacts for this surgery?

- Yes/No: Are you using a Medicare-enrolled supplier (or your plan’s required network if you have Medicare Advantage)?

- Yes/No: Did you ask for a written “covered vs upgrade” breakdown?

Neutral next step: If you answered “No” to any item, pause the purchase and fix that one thing first.

3) Coverage boundaries: what Medicare will pay for (and where it stops)

This is where the confusion usually lives: Medicare covers something real—but it’s not “whatever looks good on the display wall.” The benefit is designed to cover a standard corrective need after surgery, not every premium preference a human heart can desire (and I say that as someone who has fallen for frames that cost more than my first car payment).

Standard frames: what “standard” means in real life

“Standard frames” typically means a basic frame option that fits within Medicare’s allowed coverage parameters. If you choose a higher-priced frame, you may be responsible for the difference. The key is: you want the supplier to separate what’s covered from what’s upgraded—clearly, on paper.

Lenses basics: covered vs. add-ons that trigger out-of-pocket

Your prescription lenses themselves are the center of the post-cataract correction. But add-ons can change the bill quickly: upgraded lens designs, specialty coatings, tinting, or features marketed as “must-have” may be treated as upgrades. If you want a plain-language map of what typically turns into an add-on charge, read premium lens upgrades that can spike the bill before you’re standing under fluorescent lights nodding “sure.”

- Usually straightforward: a basic prescription lens needed after surgery

- Often an upgrade conversation: progressives, special coatings, photochromic/tints, premium “thin” options

- Almost always extra: designer frames, fashion add-ons, second pairs

Does Medicare pay for “better” lenses if your doctor recommends them?

This is the question people ask in a whisper, like Medicare might be listening. The honest answer: recommendations matter medically, but coverage decisions still follow Medicare’s benefit rules and what’s considered covered vs upgraded. If a particular feature is medically necessary, ask the supplier and your clinician’s office what documentation is needed—and don’t assume “recommended” automatically equals “covered.”

A recommendation can be medically wise and still financially “extra.” Clarify before you buy.

4) The “standard frame” riddle: who decides what counts

Here’s the sneaky part: you can hear “covered” and still end up paying. Not because anyone is evil, but because “covered” often means “covered up to an allowed amount” and the rest becomes your upgrade. It’s like ordering the basic seat on a flight and then paying extra for legroom—you still got a seat; you just chose more comfort.

The supplier’s catalog vs. Medicare’s allowance (why “covered” can still cost you)

The optical supplier is the front door. Medicare’s allowed coverage is the frame of the door. If you choose something outside that frame, you pay the difference. This is why two people can buy “glasses after cataract surgery” and one pays modestly while the other pays… a lot.

Here’s what no one tells you… the “upgrade” line item is often where bills are born

“Upgrade” can show up as a polite line on a receipt that doesn’t sound like a big deal until you total it. I’ve seen people agree to three small upgrades because each one felt “only a little,” and then the final amount felt like a jump scare.

How to request a written “covered vs upgrade” split before ordering

Ask for an itemized estimate that separates:

- Covered portion: what will be billed as the post-cataract benefit

- Patient responsibility: deductible/coinsurance (if applicable)

- Upgrades: frame difference, lens enhancements, optional coatings or features

If the estimate is vague (“you’ll owe about…”), ask again. Clear paperwork now saves hours of phone calls later. And if you want to understand why some “small” line items balloon into a larger statement later, this breakdown of a typical cataract surgery bill and common surprises will feel familiar in the best (most preventable) way.

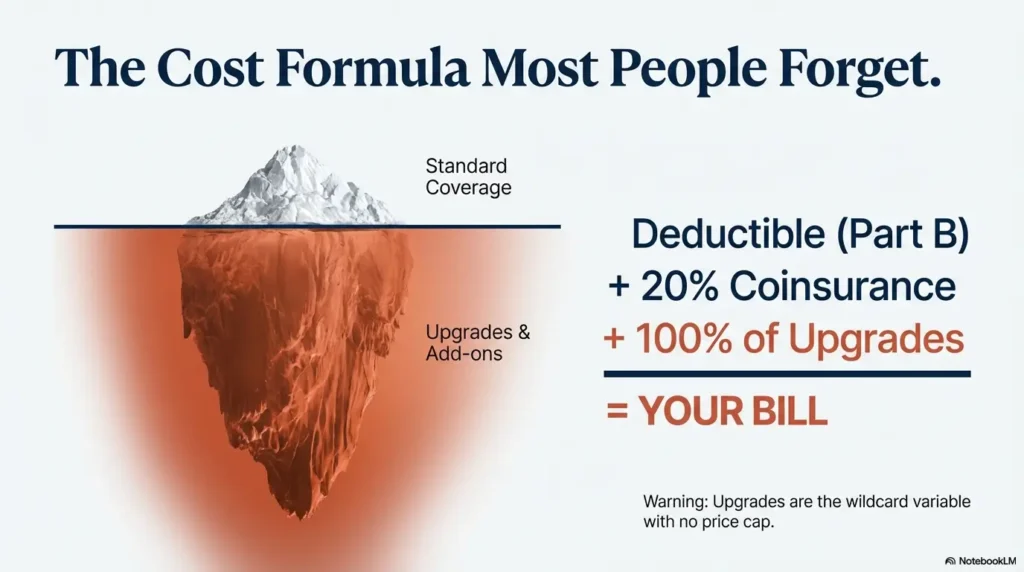

5) Money math: the cost formula most people don’t run

Medicare billing can feel like a concert hall where the music is beautiful but the program notes are missing. The goal isn’t to become a billing expert—it’s to run a simple cost formula before you swipe your card.

Part B deductible + 20% coinsurance (typical structure)

Under Original Medicare Part B, you generally pay the deductible (if not yet met) and then a percentage coinsurance for covered items. The post-cataract eyewear benefit often follows that structure, based on Medicare-approved amounts—not necessarily the sticker price. If you want the broader context for how this cost-sharing shows up across cataract-related services, see cataract surgery and Medicare Part B: what’s covered and what’s cost-sharing.

| Item (2026) | Typical range | Notes |

|---|---|---|

| Part B deductible | Applies if not met | If you’ve already met it for the year, this piece may be $0 for the eyewear claim. |

| Coinsurance | Often 20% of Medicare-approved amount | This is separate from any upgrade costs the supplier lists. |

| Upgrades | Varies widely | Designer frames, specialty lenses, coatings, tinting often land here. |

| Medigap/secondary coverage | Plan-dependent | Some Medicare Supplement plans may reduce your Part B coinsurance, but they don’t usually turn upgrades into covered items. |

Neutral next step: Ask the supplier which line items are “covered claim” vs “upgrade,” then match that to your plan type.

Assignment matters: when “doesn’t accept assignment” can change your cost

“Accepting assignment” is a billing detail that can quietly control your out-of-pocket. If a supplier accepts assignment, they agree to Medicare’s allowed amount and bill Medicare directly. If they don’t, your cost can become harder to predict. This is a “ask one question, save one headache” moment.

Why two people get the same glasses and pay wildly different amounts

Usually it’s a mix of three things:

- Deductible status: met vs not met

- Supplier billing: assignment/participation/enrollment

- Upgrade choices: frame and lens enhancements

Show me the nerdy details

Medicare often calculates payment based on Medicare-approved amounts. A supplier’s retail price can be higher than that. The difference between “approved amount,” “assignment,” and “upgrade” is where surprise bills usually come from.

This quick estimator is intentionally simple. It does not store data. It helps you ballpark the Part B coinsurance portion for the covered amount (upgrades not included).

Neutral next step: Use the estimate to sanity-check the bill, then compare it to the supplier’s itemized quote.

6) Timing traps: when to order (and when to wait)

After surgery, your eyes are doing a quiet, complicated settling process. The temptation is to order new glasses the moment you can see the clock clearly again. But ordering too early is one of the easiest ways to turn a “covered benefit” into “I paid twice.”

One-eye now, second-eye later: planning if surgeries are staged

Many people have cataract surgery on one eye first, then the other eye later. That timeline matters because your prescription can shift between surgeries. If you buy glasses after the first eye, your second surgery may change the overall balance—sometimes enough to want a new pair.

- If surgeries are close together: consider waiting for the second eye so you buy once.

- If the gap is long: you may need a practical “bridge solution” so daily life is workable.

Prescription stability: when post-op refraction usually makes sense

Your clinician will guide you on when your refraction is stable enough for a new prescription. Follow that guidance. It’s not about perfection; it’s about avoiding the “my vision changed right after I bought these” spiral.

If you order too early and your Rx changes, can you “redo” the pair?

Sometimes suppliers have remake policies; sometimes they don’t. Medicare’s benefit rules don’t automatically guarantee a redo if the prescription changes. This is why timing and written policies matter.

A friend of mine—hyper-competent, spreadsheet person, the kind who carries a pen “just in case”—had cataract surgery on her right eye and felt amazing. Two days later she walked into an optical shop with that fresh optimism and picked frames that made her look like herself again. She signed for a couple of upgrades (“only a little more”), paid, and left proud of her efficiency.

Three weeks later, her left eye surgery happened. Her vision improved, but the balance changed. Suddenly the new glasses felt slightly off—like a song half a beat late. The shop offered a partial remake policy, but it didn’t cover everything, and Medicare wasn’t going to magically fund a do-over. She wasn’t mad at anyone; she was mad at the timeline. The lesson wasn’t “never buy after the first surgery.” It was: buy with the next surgery in mind.

Timing isn’t a detail. Timing is the difference between one purchase and two.

7) Supplier rules: where people accidentally void the benefit

The most painful stories I hear are not “Medicare didn’t cover it.” They’re “Medicare would have covered it, but I bought it the wrong way.” This is where the DMEPOS supplier world (Durable Medical Equipment, Prosthetics, Orthotics, and Supplies) quietly steps onto the stage.

Use a Medicare-enrolled supplier (and confirm it’s billed correctly)

For Original Medicare, the supplier’s enrollment status matters. If the supplier can’t bill Medicare properly for the post-cataract eyewear benefit, you may end up paying retail. Ask directly: “Are you Medicare-enrolled, and do you bill the post-cataract eyewear benefit?”

Proof-of-delivery & paperwork basics (why receipts matter in coverage world)

Keep the estimate, final receipt, and any paperwork showing what was covered vs upgraded. If questions arise later—especially if there’s a billing correction—you want clean documentation, not foggy memory.

Let’s be honest… the optical shop may assume you’re paying retail unless you say the right sentence

Optical shops serve many kinds of customers: private insurance, vision plans, cash-pay, Medicare Advantage networks, and Original Medicare. Unless you clearly state your intent, the default workflow may be retail. It’s not personal. It’s just throughput.

Show me the nerdy details

Claims for post-cataract eyewear are often routed through the supplier side of Medicare billing. That’s why “who you buy from” can matter as much as “what you buy.” If you have Medicare Advantage (Part C), the plan’s network and rules may override the typical Original Medicare workflow.

- Confirm the supplier can bill Medicare for post-cataract eyewear

- Ask for itemization: covered vs upgrades

- Keep receipts and paperwork

Apply in 60 seconds: Say “post-cataract Part B eyewear benefit” before you browse frames.

8) Common mistakes: the 7 expensive misreads

This is the section you read like a pilot reads a pre-flight checklist: calmly, not because you expect disaster, but because you respect how small oversights become big costs. I’ve made two of these mistakes myself—mostly from being “helpful” and trying to move fast.

Mistake #1: assuming “one pair” means one per eye per year

The benefit is tied to cataract surgery with IOL implantation—not a calendar year and not a general “vision allowance.”

Mistake #2: buying premium frames first, asking questions later

Choose what you want—just understand what you’re paying for. Premium frames may be partially or entirely outside the covered portion.

Mistake #3: expecting replacements, backups, or sunglasses to be covered

Medicare’s vision device coverage is narrow. Replacement frames and routine eyewear typically aren’t covered the way people assume. If you want a backup pair, plan for it as an elective purchase unless your plan clearly states otherwise.

Mistake #4: using a non-participating/non-enrolled supplier

You can buy glasses anywhere. But if the supplier can’t bill the benefit properly, you may pay full price even though you “qualified.”

Mistake #5: confusing Original Medicare vs Medicare Advantage (different plan rules, different workflows)

Medicare Advantage (Part C) plans often have their own networks and vision benefits. Sometimes they offer more routine vision coverage than Original Medicare; sometimes the network rules are stricter. If you have Medicare Advantage, treat your plan documents like the boss fight—not the rumor mill.

Mistake #6: not requesting a “covered vs upgrade” breakdown in writing

Spoken explanations fade. Paperwork lasts. Get the split in writing before you commit.

Mistake #7: forgetting the deductible/coinsurance piece

Even when something is covered, you may still owe cost-sharing. When people feel “surprised,” it’s often not that Medicare paid $0—it’s that they expected $0.

- You can use a Medicare-enrolled supplier who bills the post-cataract benefit

- You want predictable Part B-style cost sharing

- You have a Medigap plan that reduces coinsurance

- Your plan includes routine vision benefits beyond post-cataract coverage

- You’re comfortable staying in-network for eyewear

- You want a bundled plan experience (and can follow plan rules)

Neutral next step: Check whether your plan requires a specific network supplier before you order anything.

FAQ

Does Medicare cover glasses after cataract surgery with an IOL?

Under Original Medicare Part B, there is typically a narrow benefit for corrective lenses after cataract surgery with an implanted intraocular lens (IOL). It’s not routine vision coverage; it’s a post-surgery exception.

Is it one pair per eye or one pair per surgery?

The benefit is generally described as applying after each cataract surgery that implants an IOL. If surgeries are staged (one eye, then the other), treat them as separate events for planning purposes.

Can I choose contacts instead of glasses?

Typically, you choose either eyeglasses with standard frames or contact lenses for that post-surgery benefit. If you strongly prefer contacts, decide early so the supplier bills correctly.

Does Medicare cover premium lenses (progressives, blue-light, photochromic)?

Many premium features are treated as upgrades. Coverage can depend on how the item is classified and billed. Ask for a written breakdown that separates the covered portion from upgrade costs before you buy. If you want to walk in with names, not vibes, review which premium lens upgrades are usually “extra” so you can choose intentionally.

Will Medicare pay for designer frames if I pay the difference?

Often, yes in the practical sense: you may be able to apply the covered portion toward standard frames and pay the difference for a premium frame. But the exact process depends on supplier billing and itemization—get it in writing.

What if I break the glasses—will Medicare replace them?

Replacement coverage is often limited. Don’t assume the post-cataract benefit functions like an ongoing warranty. If you want protection, ask the supplier about separate breakage or remake policies (and keep your paperwork).

Do I have to use a Medicare-enrolled supplier?

For Original Medicare billing, supplier enrollment and proper claim submission matter. If you have Medicare Advantage, your plan may require a specific network supplier instead.

How much will I pay out of pocket with Part B?

Many people owe some combination of deductible (if not met), coinsurance, and any upgrade costs. The mini calculator above can help you ballpark the covered portion, but upgrades can change the final number. If you want a broader “why did my total look like that?” explainer, this walkthrough of a cataract surgery bill and post-op costs pairs well with the eyewear math.

Does Medicare Advantage cover more than “standard frames”?

Some Medicare Advantage plans include routine vision benefits that Original Medicare doesn’t. But they may also require in-network providers and prior steps. Check your plan’s evidence of coverage before ordering.

What if my surgery was years ago—can I claim the benefit now?

Claim timing and documentation can matter, and rules can differ by plan and supplier process. If you’re in this situation, call your plan (or Medicare, if applicable) and ask what documentation is needed and whether a retroactive claim is possible.

10) Next step: one action that prevents 80% of surprise bills

If you only do one thing from this article, do this: say the benefit out loud, early, before you browse frames. It changes which workflow you enter—and the workflow determines the bill.

Use this one-liner at the optical shop:

“I’m using my post-cataract Part B eyewear benefit—please itemize what Medicare covers vs what I’d pay as upgrades, and confirm you’re a Medicare-enrolled supplier.”

- Say the benefit name early

- Demand itemization

- Confirm supplier/network rules

Apply in 60 seconds: Screenshot the script and keep it in your phone notes.

Conclusion

Let’s close the loop from the beginning: Medicare’s “one pair of glasses” rule is real—but it’s not a blank check. It’s a narrow, post-cataract benefit tied to an implanted lens, and it works best when you treat it like a process: right timing, right supplier, and a clean “covered vs upgrade” breakdown before you commit.

Cataract surgery with an implanted lens (IOL).

Follow clinician guidance for prescription timing.

Glasses (standard frames) or contacts.

Confirm supplier enrollment/network + get itemization.

Accessibility note: This infographic shows a four-step flow from surgery to a properly billed eyewear purchase.

If you’re time-poor (and who isn’t), here’s the 15-minute version: call the optical shop, ask if they’re Medicare-enrolled (or in-network for your Medicare Advantage plan), and request an itemized estimate before you go in. Bring that estimate with you. Then you can choose frames with joy instead of suspicion—which is how shopping should feel.

Friendly note: This article is educational and not medical, legal, or financial advice. Coverage details can vary by plan type, supplier, and billing circumstances. (And if you’re still in the “recovery logistics” window, pairing this with best home setup after cataract surgery can make the first week feel a lot less improvisational—especially while you’re waiting for your prescription to settle.)

Last reviewed: 2026-01.